Rental property owners in Minnesota face real financial exposure when accidents happen on their premises. A single slip-and-fall lawsuit or tenant-caused damage can cost tens of thousands of dollars in legal fees and settlements.

Liability insurance for rental property protects you from these unexpected costs. At Variant Insurance Group, we help property owners understand what coverage they actually need and how to avoid expensive gaps in protection.

What Liability Coverage Actually Protects

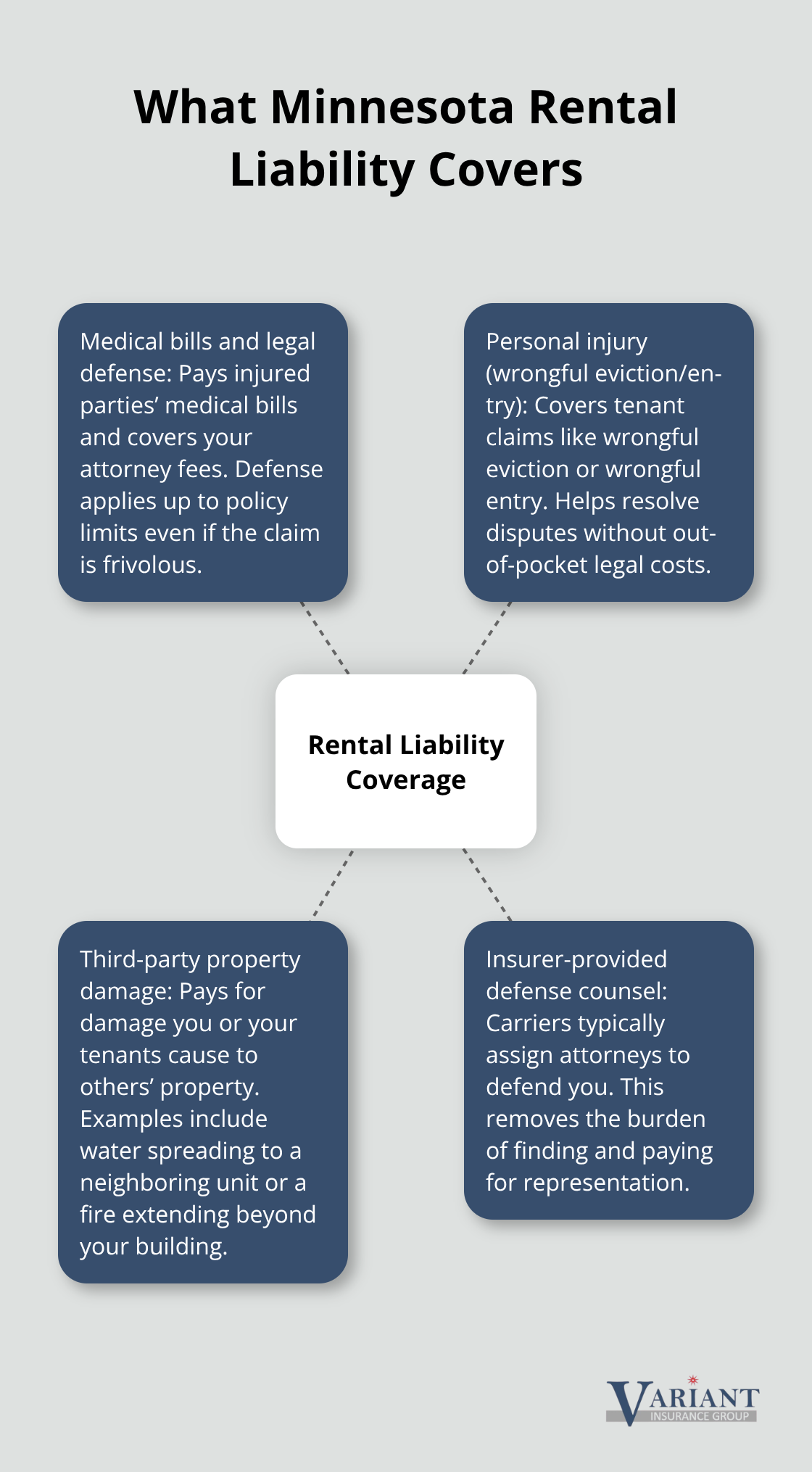

Liability insurance for rental property covers two critical areas that can devastate your finances if left uninsured. First, it pays medical expenses and legal defense costs when someone is injured on your property and holds you responsible. According to the Insurance Information Institute, this includes slip-and-fall accidents, dog bites, or injuries caused by maintenance negligence like a loose handrail or exposed sprinkler head. The policy covers your legal defense up to the policy limits, which matters because defending yourself against even a frivolous claim can cost $5,000 to $15,000 in attorney fees alone. Second, liability coverage protects you if you or your tenants cause damage to someone else’s property, such as water damage that spreads to a neighboring unit or fire that extends beyond your building.

Medical Expenses and Legal Defense

When a tenant or guest is injured on your property, your liability coverage pays their medical bills and covers your legal costs if they sue. This protection matters because Minnesota renters occupy over 27% of housing units, meaning significant foot traffic moves through your property regularly. A single slip-and-fall case can result in claims ranging from $10,000 for minor injuries to $100,000 or more for serious ones. Your policy also covers personal injury claims related to wrongful eviction or wrongful entry, which protects you from expensive tenant disputes that can drag on for months. Insurers typically assign attorneys to defend you, removing the burden of finding and paying for representation out of pocket.

Property Damage Your Tenants Cause

Liability coverage protects you when tenants or their guests damage property beyond normal wear and tear. This includes fire damage caused by tenant negligence, water damage from a tenant leaving a bathtub running, or damage to neighboring properties caused by tenant actions. Many property owners mistakenly believe their standard landlord policy covers all tenant-caused damage, but liability specifically addresses third-party claims and damage to others’ property. If a tenant’s negligence causes a fire that damages the adjacent unit, your liability coverage pays the neighbor’s claim. Without this protection, you personally absorb the cost of repairs and any liability judgment against you.

Understanding Your Coverage Limits

Your coverage limits determine the maximum amount your insurer pays for a single claim or all claims in a policy year. Coverage limits typically range between $100,000 and $1,000,000 per occurrence, though your property value and local risk factors should guide this decision. A serious injury claim can easily exceed $50,000 when medical costs, lost wages, and pain-and-suffering damages combine. Setting limits too low leaves you exposed to personal liability for amounts above your policy maximum. The cost difference between a $100,000 limit and a higher limit is often modest, making higher limits a practical choice for most rental properties.

Why Liability Gaps Cost You Money

Standard homeowners insurance does not cover rental properties because insurers design those policies for owner-occupied homes. Attempting to use homeowners coverage on a rental property creates a dangerous gap-your insurer can deny claims or cancel your policy if they discover the property is rented. Landlord liability policies exist specifically to address the unique risks of rental operations, including higher tenant turnover and increased exposure to injury claims. Skipping proper liability coverage or underestimating your limits transforms a manageable insurance expense into a financial catastrophe when accidents happen. The next section examines the specific liability claims that rental property owners face most often.

Common Liability Claims Rental Property Owners Face

Slip-and-Fall Accidents in Minnesota Properties

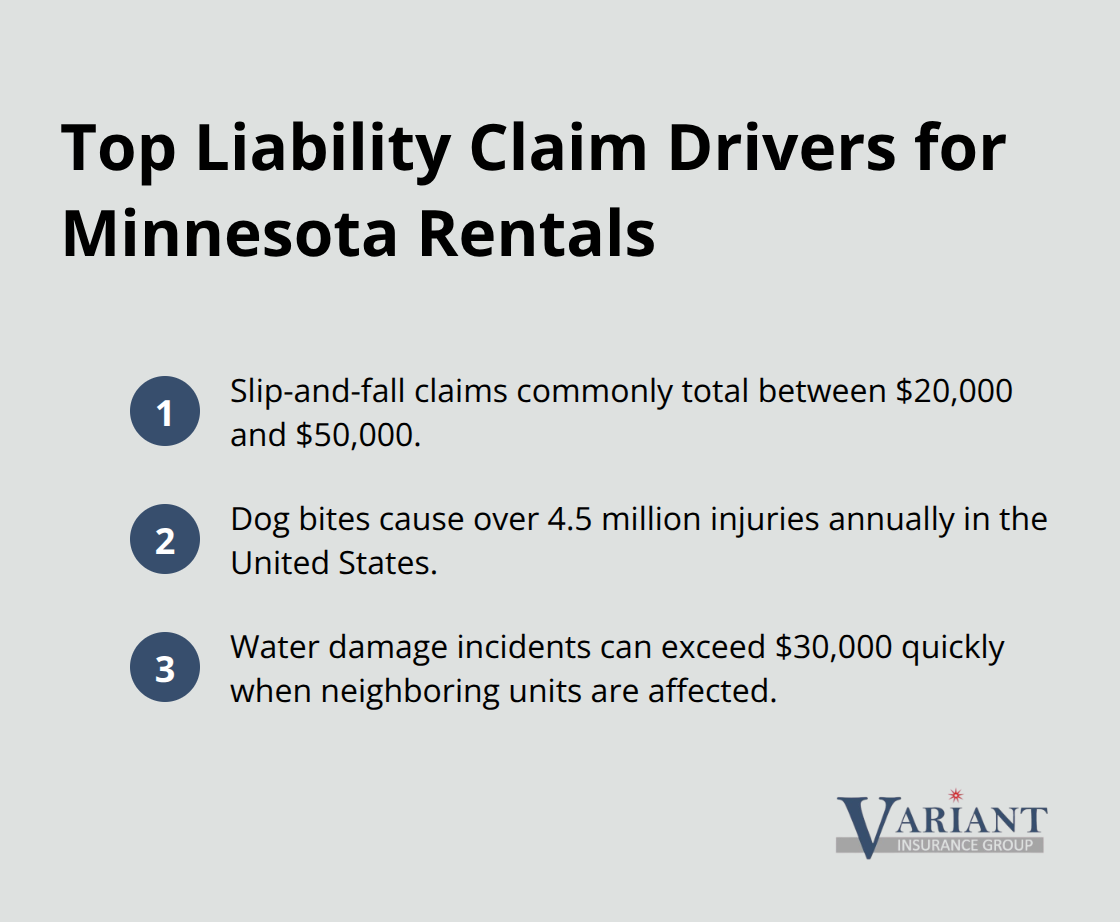

Slip-and-fall accidents represent the most common liability claim rental property owners face in Minnesota. A tenant trips on a loose stair, a guest slips on wet flooring in a hallway, or someone falls because of poor lighting in a common area-these scenarios happen regularly and trigger expensive lawsuits. Slip-and-fall claims average between $20,000 and $50,000 when medical costs, lost wages, and legal fees combine. Minnesota winters amplify this risk significantly. Icy walkways, snow-covered steps, and inadequate snow removal create hazardous conditions that invite claims. Property owners who fail to remove snow within 24 hours of a storm or neglect to salt walkways face higher liability exposure.

Your liability coverage pays the injured person’s medical bills and your legal defense costs if they sue, protecting you from absorbing these expenses personally. The key to managing slip-and-fall risk is documenting your maintenance efforts-photograph snow removal work, keep receipts for salt and sand purchases, and maintain detailed records showing when you addressed hazards. This documentation protects you if a claim arises, since it demonstrates you took reasonable precautions to prevent injuries.

Pet-Related Injuries and Your Liability

Dog bites alone result in over 4.5 million injuries annually in the United States, with homeowners and rental property liability policies covering these claims when the property owner failed to control the animal or warn visitors about the danger. Minnesota landlords who allow tenants to keep dogs face significant liability if the animal injures a guest or another tenant. Your liability policy covers the medical expenses and legal costs, but only if you took reasonable precautions like requiring pet deposits or liability waivers. Without documented safeguards, insurers may deny your claim or reduce coverage, leaving you personally responsible for medical bills and settlements.

Water Damage From Maintenance Failures

Water damage from tenant negligence or your maintenance failures creates expensive third-party claims when water leaks into neighboring units or causes structural damage. A burst pipe, overflowing bathtub, or failed sump pump can damage adjacent properties, triggering claims that exceed $30,000 quickly. Liability coverage protects you when the damage results from your negligence in maintaining the property-a leaking roof you ignored, faulty plumbing you failed to repair, or inadequate drainage around the foundation.

The most practical step is conducting thorough property inspections every three to six months, documenting the condition of plumbing, roofing, and drainage systems. Address maintenance issues immediately rather than deferring repairs, since delaying fixes increases both your liability exposure and your insurance costs. These inspections also help you identify hazards before they cause injuries or property damage, reducing the likelihood that claims occur in the first place. Understanding what your liability policy covers is only half the battle-selecting the right coverage limits and exclusions for your specific property requires careful assessment of your unique risks.

How Much Coverage Do You Actually Need

Selecting the right liability limits requires honest assessment of your property’s exposure rather than guessing or copying what other landlords carry. Minnesota rental properties range from single-family homes in quiet neighborhoods to multi-unit buildings in dense urban areas, and each carries different risk profiles. A property in a high-crime area with aging infrastructure faces higher liability exposure than a newly renovated home in a safe neighborhood.

Assess Your Property’s Specific Characteristics

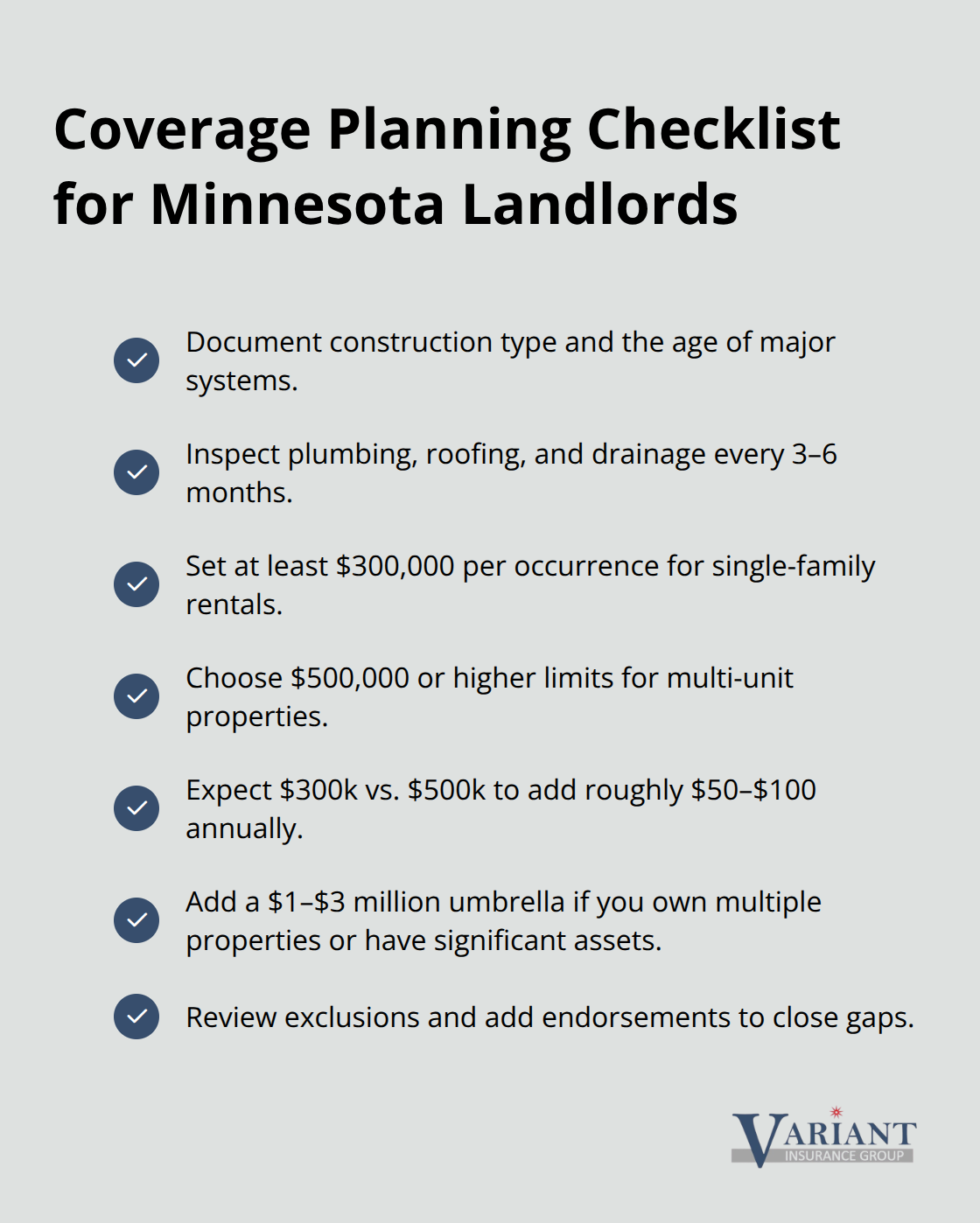

Start by documenting your property’s specific characteristics: construction type, age of major systems like plumbing and electrical, number of units, location relative to schools or parks, and local crime statistics. Properties with outdated systems invite more injury claims because maintenance failures become more likely. A building with original plumbing from the 1970s poses greater water damage risk than one with recently updated pipes. Research what similar properties in your area pay for liability claims by contacting local property managers or speaking with an independent insurance agent who can share anonymized claim data. This information grounds your coverage decision in real-world experience rather than theoretical scenarios.

Match Coverage Limits to Your Property’s Risk

Your coverage limits should reflect your property value and the potential severity of claims in your area. Coverage limits typically range between $100,000 and $1,000,000 per occurrence, though the right choice depends on your specific situation. A single serious injury claim in Minnesota can easily reach significant amounts when medical costs, lost wages, and legal defense combine, so $100,000 limits often prove inadequate for properties with significant tenant traffic. Minimum coverage of $300,000 per occurrence works well for single-family rentals and $500,000 or higher for multi-unit properties. The cost difference between $300,000 and $500,000 in coverage is typically $50 to $100 annually, making higher limits a practical investment.

Consider Umbrella Liability Protection

Beyond your primary liability policy, consider umbrella liability insurance in the $1,000,000 to $3,000,000 range if you own multiple properties or have significant net worth to protect. Umbrella policies cost $150 to $300 annually and provide critical protection when a major claim exceeds your underlying policy limits. This additional layer of coverage prevents a catastrophic claim from wiping out your personal assets and investment returns.

Identify and Close Coverage Gaps

Review your policy exclusions carefully because gaps in coverage create dangerous blind spots. Many standard policies exclude intentional damage, damage from vacant properties after 30 days, or claims related to certain property conditions. Discuss these exclusions with your agent and add endorsements for protections you need, such as coverage for temporary vacancy periods or enhanced water damage protection. An independent insurance agent can shop multiple carriers to compare which exclusions matter most for your property and which insurers offer the flexibility you require.

Final Thoughts

Liability insurance for rental property protects your financial future when accidents happen on your premises. The stakes are real in Minnesota, where slip-and-fall claims, water damage, and tenant-related injuries can cost tens of thousands of dollars in medical expenses and legal defense. Setting appropriate coverage limits, documenting your maintenance efforts, and closing policy gaps separates property owners who recover from claims versus those who face personal financial ruin.

Your next step is obtaining quotes from multiple carriers to compare coverage options and pricing. Minnesota’s rental market demands serious protection, and the cost difference between inadequate coverage and comprehensive protection is often just $50 to $100 annually. An independent insurance agent can shop carriers on your behalf, identifying which insurers offer the flexibility and coverage your property needs without forcing you into unnecessary add-ons.

We at Variant Insurance Group specialize in helping Minnesota property owners find the right liability insurance for rental property by comparing options from top-rated insurers in the state. Our team reviews your property details, assesses your liability exposure, and presents coverage options with transparent pricing so you can make informed decisions. Contact us today to discuss your rental property’s liability insurance needs and get quotes that fit your budget and risk profile.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation