Running a business with vehicles means managing real risks on Minnesota roads. Commercial auto insurance isn’t optional-it’s a legal requirement that protects your company from accidents, injuries, and property damage claims.

At Variant Insurance Group, we help Minnesota business owners find policies that match their fleet size and budget. The right coverage keeps your operations running smoothly when unexpected incidents happen.

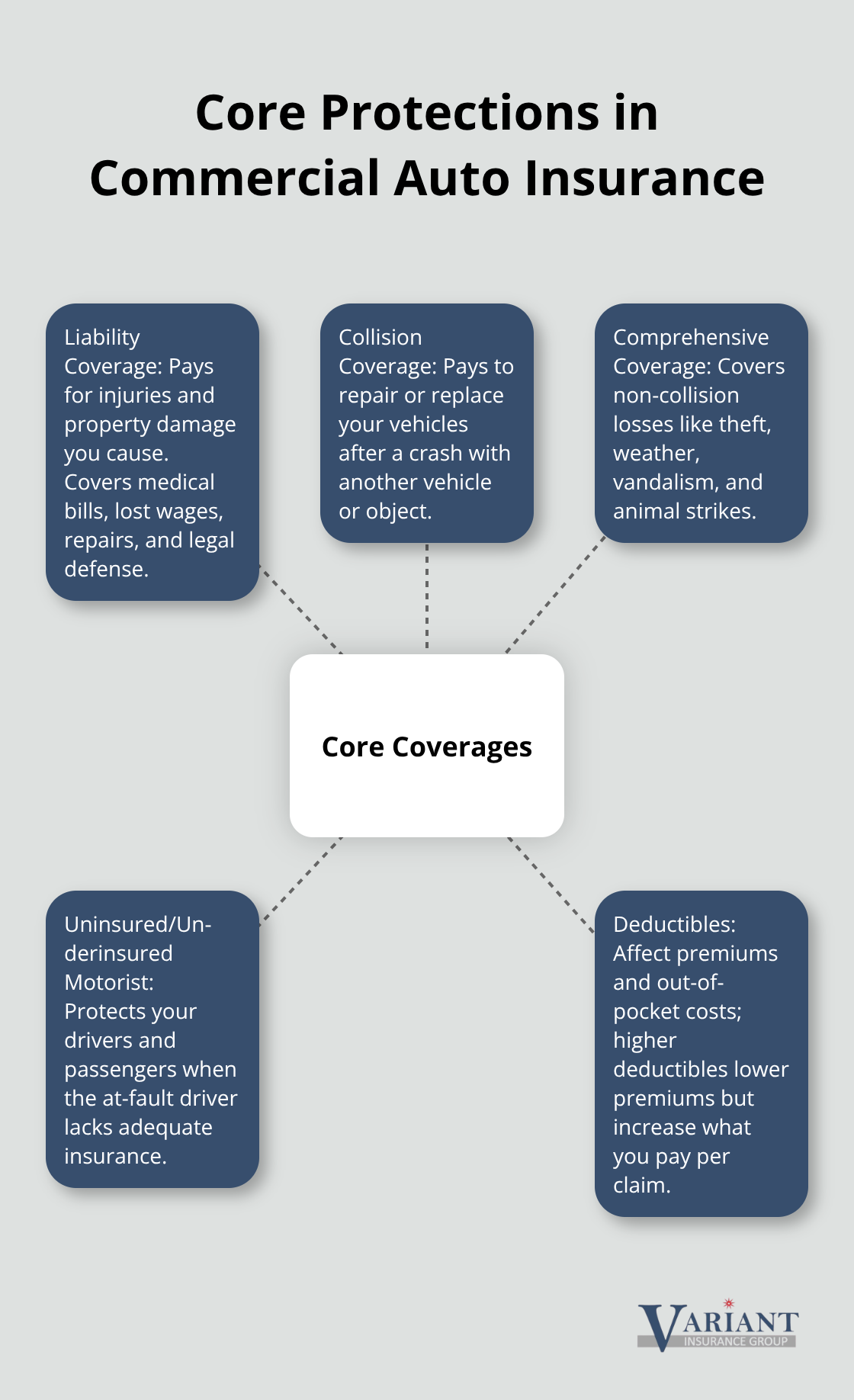

What Commercial Auto Insurance Actually Covers

Minnesota law requires specific liability minimums that form the foundation of commercial auto insurance. You need at least Minnesota’s required liability minimums of $30,000 per person and $60,000 per accident for bodily injury liability, plus $10,000 for property damage liability. These minimums exist because accidents happen frequently on Minnesota roads, and a single serious collision can generate costs far exceeding these thresholds. Many businesses operate with exactly these minimums, which is a mistake. A catastrophic accident involving multiple vehicles or serious injuries can easily reach $250,000 to $500,000 in damages.

At that point, your business assets become vulnerable to lawsuits. Liability coverage protects you when you’re found responsible for injuries or damage to someone else’s property. It covers medical bills, lost wages, vehicle repairs, and legal defense costs. The coverage applies regardless of whether you caused the accident or your driver did, as long as they operated a company vehicle for business purposes.

Liability Coverage Forms Your First Line of Defense

Liability coverage pays for the other party’s expenses when your business is at fault. This protection extends to bodily injury claims and property damage claims separately. Medical bills from a serious accident can exceed $100,000 quickly, especially if multiple people suffer injuries. Legal defense costs add another substantial burden if the injured party sues your business. Without adequate liability limits, a single accident can threaten your company’s financial stability and force you to liquidate assets to settle claims.

Physical Damage Protection Prevents Operational Disruption

Collision and comprehensive coverage protect your own vehicles from damage. Collision covers accidents with other vehicles or objects. Comprehensive covers theft, weather, vandalism, and animal strikes. Many Minnesota businesses skip these coverages on older vehicles, assuming they’ll replace them if damaged. This approach backfires when a vehicle sustains damage but remains operational. A single accident involving a commercial truck can cost $15,000 to $30,000 in repairs, depending on the vehicle and damage severity. Repair costs have climbed significantly due to modern safety systems and supply chain delays. Comprehensive coverage prevents a weather event like hail or a break-in from derailing operations. Without it, you absorb the full cost of repairs immediately.

Deductibles Shape Your Premium and Out-of-Pocket Costs

The deductible you choose directly affects your premium and out-of-pocket costs. A $1,000 deductible is standard but costs more monthly. A $2,500 deductible reduces premiums substantially if your drivers maintain clean records and you operate in lower-risk areas. For example, with a $1,000 vehicle damage claim and a $250 deductible, you pay $250 and the insurer pays the remaining $750. Higher deductibles work well for businesses with strong safety records and stable operations.

Uninsured Motorist Coverage Protects Against Gaps

Uninsured and underinsured motorist coverage protects your drivers and passengers when another driver lacks adequate insurance. Minnesota roads include drivers without proper coverage, and an accident with an uninsured driver leaves you exposed. This coverage pays for medical expenses, lost wages, and vehicle damage when the at-fault party can’t cover costs. It’s especially important if your drivers spend significant time on highways or in high-traffic areas where accident severity tends to be higher. This protection ensures your team receives compensation even when the other driver cannot pay.

Understanding what your policy covers is only half the battle. The next step involves recognizing why Minnesota businesses cannot operate without this protection, both legally and financially.

Why Your Minnesota Business Cannot Operate Without Commercial Auto Insurance

Legal Requirements Demand Coverage

Minnesota law mandates commercial auto insurance for any vehicle operated for business purposes. Operating a service van, delivery truck, or fleet without liability coverage violates state law and exposes you to criminal penalties, license suspension, and civil liability. The state requires minimum liability limits of $100,000 in Minnesota. These minimums form a legal floor, not a safety ceiling.

Accident Costs Exceed What Most Businesses Expect

The financial reality of accidents in Minnesota demands robust protection. A 2024 analysis from CBIZ showed that commercial auto insurers posted combined loss ratios above 100 percent, meaning claims and expenses exceeded earned premiums. This trend reflects the severity and frequency of accidents on Minnesota roads.

Medical costs spiral quickly after a serious collision. A single accident involving multiple people can generate $200,000 to $500,000 in medical bills, lost wages, and property damage within days. Without adequate liability coverage, your business absorbs these costs directly, threatening payroll and operations. One accident with a significant injury can bankrupt a small business that skimped on coverage limits.

Vehicle Damage Disrupts Operations and Drains Cash

Modern commercial vehicles cost $40,000 to $150,000 depending on type and specifications. Repair costs have climbed substantially due to advanced safety systems and ongoing supply chain delays. A collision involving driver-assistance systems costs twice as much to repair as older vehicles.

When your vehicle sustains damage and sits in a repair shop for weeks, your business loses revenue. Comprehensive and collision coverage ensures repairs happen quickly without depleting cash reserves. Physical damage protection prevents operational disruption and keeps your fleet moving.

Coverage Gaps Create Expensive Surprises

Coverage for multiple vehicles and different driver situations prevents gaps that catch business owners off guard. If your employees occasionally use personal vehicles for business, your personal auto policy typically excludes business use. This creates a coverage void that exposes you to liability without protection.

Leased vehicles, rented equipment vehicles, and non-owned vehicles all require explicit coverage confirmation with your insurer. Many Minnesota businesses discover mid-claim that their policy doesn’t cover a specific vehicle or driver situation, resulting in denied claims and out-of-pocket costs. A thorough conversation with your insurer about all vehicles and driver scenarios prevents these expensive surprises.

Market Conditions Make Coverage Harder to Obtain

The market hardening trend affecting Minnesota fleets means rates are rising and insurers are tightening underwriting standards. Carriers have withdrawn coverage from higher-risk operations, making it harder to obtain affordable protection. Securing the right policy now, while market conditions allow, protects your business from future rate shocks and coverage denials. Understanding what coverage you need is only the first step-selecting the right policy from available options requires careful comparison of limits, deductibles, and additional protections tailored to your specific fleet.

Selecting Coverage That Matches Your Real Fleet Operations

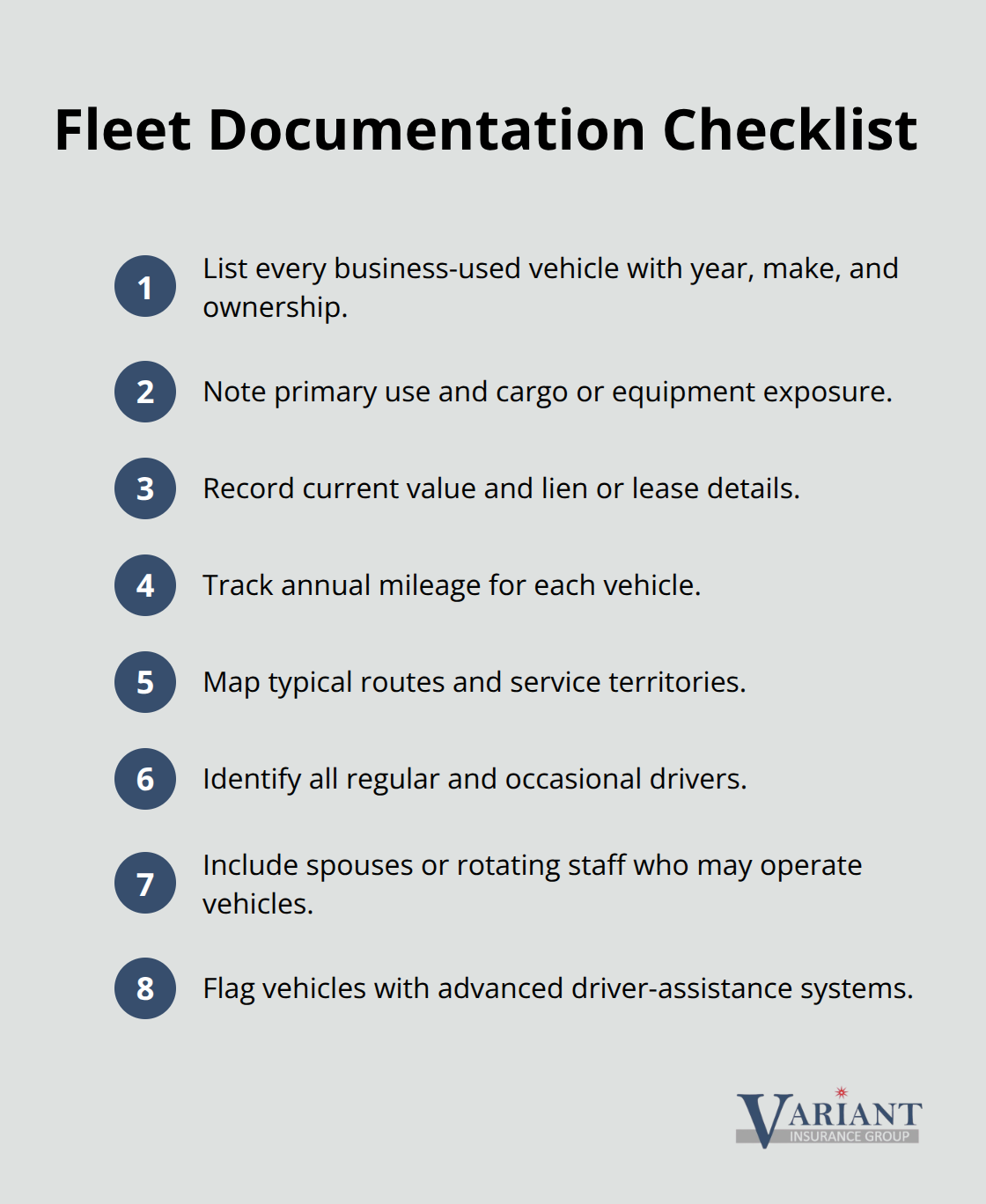

Catalog Your Vehicles and Document Operational Patterns

Start with an honest assessment of every vehicle used for business, including ownership status, age, value, and primary use. A contractor operating a 2022 pickup truck faces fundamentally different coverage needs than a food service business running three delivery vans and a catering truck. The pickup truck may require only liability and collision coverage, while the food operation demands additional consideration for cargo exposure and multiple driver situations.

Document annual mileage for each vehicle because insurers adjust premiums based on exposure. A delivery service logging 50,000 miles annually across Minnesota highways encounters different risk than a local plumber making short trips within a single county. Geographic patterns matter significantly-highway driving through rural Minnesota presents different accident dynamics than urban delivery routes. Be specific about who drives each vehicle.

If three employees rotate driving company vans, all three must appear on the policy. If your spouse occasionally uses a business vehicle, that usage needs explicit coverage. Omitting drivers creates coverage gaps that surface during claims, leaving your business exposed.

Evaluate Liability Limits Beyond Legal Minimums

Coverage limits require honest evaluation of your liability exposure, not acceptance of legal minimums. Minnesota requires $30,000 per person and $60,000 per accident for bodily injury liability, but these minimums leave your business vulnerable. A serious accident involving multiple vehicles can generate $250,000 in damages within hours. Consider your business assets when selecting limits. A contractor with $500,000 in equipment and vehicles should carry liability limits reflecting potential loss scenarios. Many Minnesota businesses operate with $100,000 liability limits, which provides reasonable protection for smaller operations but remains inadequate for larger fleets.

Compare Deductibles and Physical Damage Protection

Compare deductibles across three to five providers because premium differences can reach 20 to 30 percent for identical coverage. A $2,500 deductible reduces your monthly premium substantially compared to a $500 deductible, but only if your drivers maintain clean records and you operate in established service areas. If your drivers include younger employees or those with recent violations, higher deductibles create unmanageable out-of-pocket costs when accidents occur.

Physical damage coverage deserves equal attention. Collision and comprehensive protection prevent a single incident from derailing operations. Modern commercial vehicles cost $40,000 to $150,000, and repair expenses have climbed significantly due to advanced safety systems and supply chain delays. Vehicles with driver-assistance systems cost twice as much to repair after collisions. Evaluate whether your business can absorb a $20,000 repair bill immediately or whether physical damage coverage makes financial sense.

Address Industry-Specific Coverage Gaps

Additional coverage options depend on your specific industry and operational details. Businesses with employees driving personal vehicles for work should confirm coverage for non-owned vehicles. Leased vehicles require explicit coverage confirmation with your insurer before assuming protection applies. Food service operations need separate general liability coverage for food-related risks because commercial auto insurance excludes food spoilage and foodborne illness claims. Many Minnesota businesses discover too late that their policy excludes a regular driver or specific vehicle type, resulting in denied claims and unexpected out-of-pocket costs.

Final Thoughts

Commercial auto insurance in Minnesota protects your business from financial devastation when accidents happen on the road. The coverage you select today determines whether your company survives a serious collision or faces bankruptcy from medical bills, legal costs, and vehicle repairs. Legal minimums provide a starting point, but they leave your business vulnerable to catastrophic losses that exceed those thresholds regularly.

Your next step is straightforward: gather information about every vehicle your business operates, document who drives them, and assess your liability exposure honestly. Compare coverage limits and deductibles across multiple providers because premium differences can reach 20 to 30 percent for identical protection. Evaluate whether your current policy covers all vehicles and drivers, or whether gaps exist that could trigger denied claims when you need protection most.

We at Variant Insurance Group work with Minnesota’s top-rated insurance companies to find policies that match your fleet size, budget, and operational reality. Contact Variant Insurance Group to discuss your commercial auto insurance needs and receive personalized recommendations tailored to your Minnesota operations. We’re ready to help you find the right coverage so your business keeps moving forward.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation