Running a business with vehicles in Minnesota means navigating specific insurance requirements that generic policies simply don’t address. Minnesota commercial auto coverage needs to account for winter driving hazards, state liability rules, and the unique demands of your fleet.

At Variant Insurance Group, we’ve helped countless Minnesota businesses find protection that actually matches their operations. The right policy fills gaps that off-the-shelf coverage leaves wide open.

What Commercial Auto Insurance Covers in Minnesota

Minnesota commercial auto policies protect your business against the financial fallout of vehicle-related incidents, but the coverage extends well beyond simple collision repairs. Understanding what’s actually included in a standard policy helps you identify where gaps exist and what additional protection your fleet truly needs.

State Minimum Requirements and Liability Limits

Minnesota law mandates specific minimum coverage levels: $30,000 per person and $60,000 per accident for bodily injury liability, plus $10,000 for property damage. These minimums apply to all vehicles, but most Minnesota businesses operating multiple vehicles or handling valuable cargo should carry substantially higher limits to shield both company and personal assets from lawsuits.

Higher liability limits cost more in premiums, but they provide proportionally stronger protection against catastrophic claims that could otherwise devastate your business.

Vehicle Damage Protection

Collision and comprehensive coverage form the foundation of vehicle protection. Collision coverage pays to repair or replace your vehicle after an accident regardless of fault, while comprehensive handles non-collision damage like theft, vandalism, fire, hail, and weather-related destruction. In Minnesota’s harsh winters, comprehensive coverage proves invaluable-the state experiences significant ice damage, snow-related collisions, and theft losses during seasonal transitions. Your choice of deductible directly affects your premium; selecting a $1,000 deductible instead of $250 can meaningfully reduce monthly costs if your business can absorb that out-of-pocket expense.

Medical and Uninsured Motorist Protection

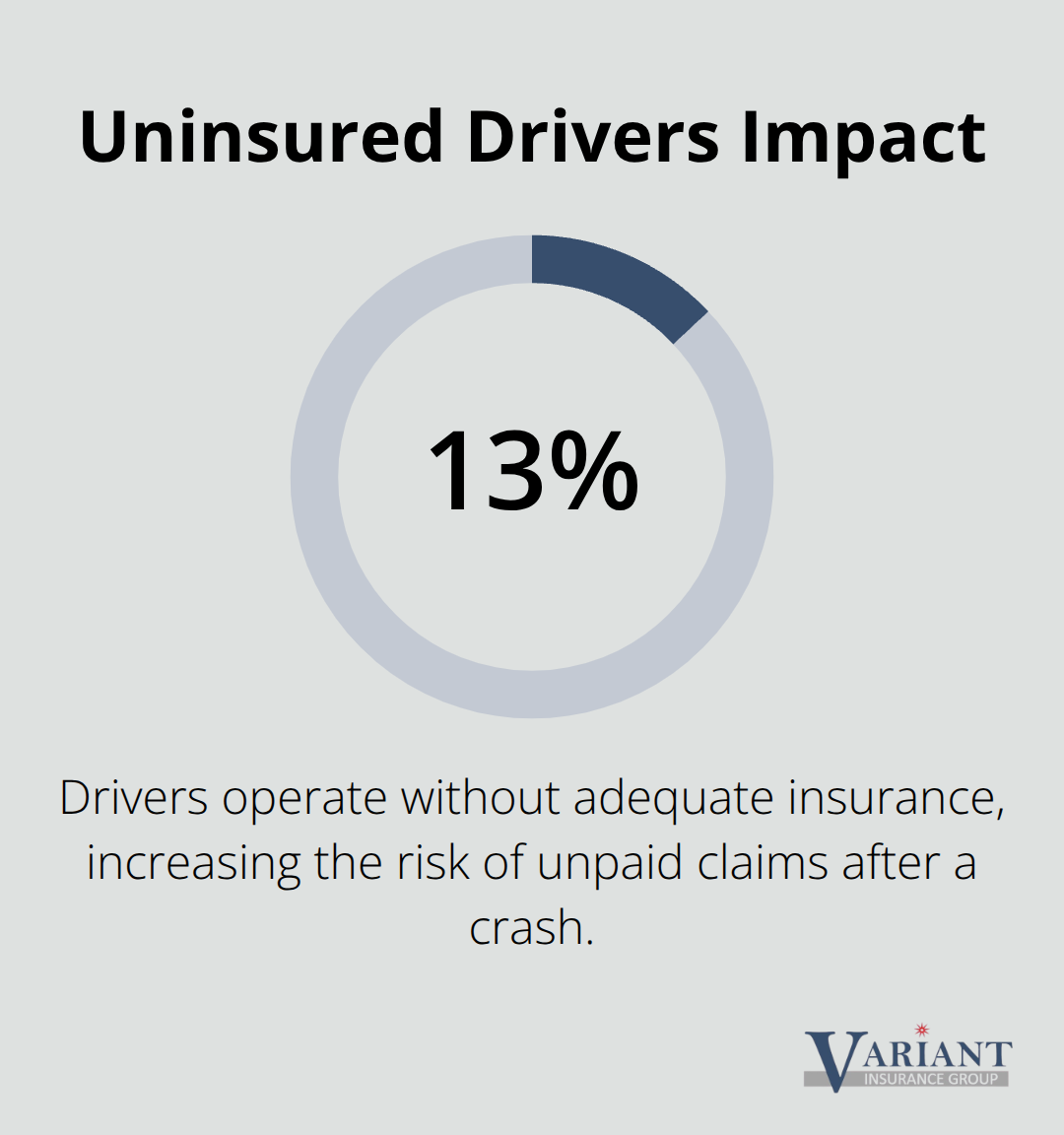

Medical payments coverage and uninsured motorist protection address the human cost of accidents. Medical payments coverage pays for injuries to you or your employees after a crash without requiring fault determination, covering hospital bills and rehabilitation expenses. Uninsured motorist coverage protects your business when the at-fault driver lacks sufficient insurance, a critical safeguard since roughly 13% of drivers nationwide operate without coverage. Minnesota requires uninsured and underinsured motorist coverage at minimum levels of $25,000 per person and $50,000 per accident, making this protection non-negotiable.

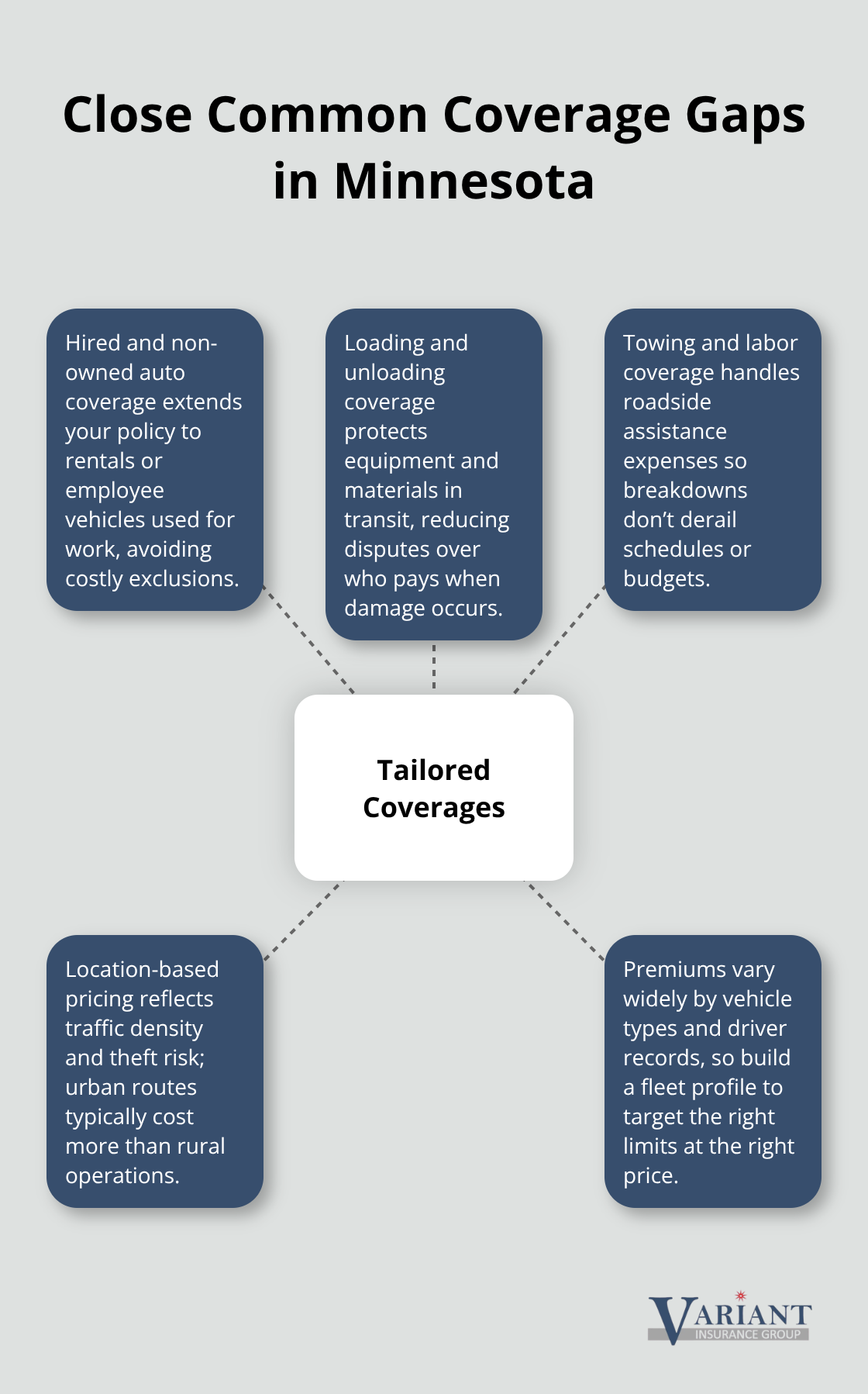

Coverage Gaps and Specialized Protection

Many Minnesota businesses find that standard commercial policies leave gaps in specialized areas. Hired and non-owned auto coverage extends protection to rental vehicles or employee personal vehicles used for business purposes, which generic policies explicitly exclude. Loading and unloading coverage protects materials or equipment during transport, while towing and labor coverage handles roadside assistance expenses. Location matters significantly within Minnesota; businesses operating in areas with higher traffic density or theft risk pay more than those in rural regions.

The average Minnesota commercial auto policy costs about $213 monthly, but pricing varies dramatically based on your vehicle types, driver records, business location, and claims history.

Understanding these coverage components reveals why one-size-fits-all policies fail Minnesota businesses. Your specific fleet size, driving patterns, and routes demand a customized approach that accounts for your actual operational risks.

Why Your Minnesota Business Needs Coverage Beyond State Minimums

State Minimums Leave Your Business Exposed

Generic commercial auto policies treat all businesses the same, which is precisely why they fail Minnesota operations. State minimum liability coverage limits of $30,000 per person and $60,000 per accident sound adequate on paper, but they collapse instantly when a serious accident involves multiple vehicles or significant property damage. A single collision causing $150,000 in injuries and vehicle damage leaves your business personally liable for the remaining $90,000 after minimums are exhausted, potentially forcing asset seizure or bankruptcy. Most successful Minnesota businesses carrying multiple vehicles or transporting goods carry liability limits of $1 million or higher, understanding that the modest premium increase delivers vastly superior protection. Your specific operational risks determine the right coverage level, not some industry average or competitor’s policy.

Winter Weather Demands Comprehensive Protection

Minnesota’s winter weather creates genuine, measurable exposures that generic policies inadequately address. The state averages 54 inches of snow annually and experiences temperatures dropping below zero for extended periods, which generates collision and comprehensive claims at rates significantly higher than national averages. Comprehensive coverage becomes non-negotiable when your fleet faces regular exposure to ice damage, snow-related accidents, theft during seasonal transitions, and hail storms. Additionally, Minnesota requires uninsured motorist coverage at $25,000 per person and $50,000 per accident because approximately 13 percent of drivers operate without adequate insurance-a real risk that affects your business directly.

Specialized Coverage Gaps in Standard Policies

Coverage gaps emerge in specialized areas where standard policies explicitly exclude protection. Hired and non-owned auto coverage protects rental vehicles or employee personal vehicles used for business purposes, while loading and unloading coverage protects transported materials. Towing assistance covers fleet vehicles stranded on Minnesota roads, and bobtail coverage protects tractors operating without trailers. Standard commercial policies leave all these exposures unprotected, forcing your business to absorb costs that tailored coverage would handle.

Location and Routes Shape Your True Risk Profile

Geographic location within Minnesota matters substantially for pricing and risk. A delivery business operating in Minneapolis faces higher theft and traffic-related claims than one based in rural areas, yet both require tailored protection matching their actual routes and exposure patterns. Your specific driving corridors, frequency of urban versus rural operations, and the neighborhoods where your vehicles park all influence which coverage options matter most. The complexity of Minnesota’s regulatory environment combined with regional weather hazards and diverse business operations means that cookie-cutter policies consistently leave dangerous gaps in your protection.

Your fleet’s actual exposure demands a customized approach that accounts for your vehicle types, driver records, and operational patterns-factors that determine whether you need higher liability limits, specialized coverage options, or both.

Building a Fleet Profile That Matches Your Actual Business

Document Your Vehicle Inventory with Precision

Choosing the right commercial auto insurance starts with an honest assessment of what your fleet actually does, not what you think it does. Many Minnesota business owners guess at their coverage needs based on competitor policies or industry assumptions, then discover midway through a claim that their protection was inadequate. Document your current vehicle inventory with specific details: how many vehicles you own versus lease, the types of vehicles (pickup trucks, vans, sedans, box trucks), their values, and their ages. A construction company operating three pickup trucks has vastly different exposure than a delivery service running eight box vans, yet both might carry similar premiums if coverage is mismatched.

Map Your Actual Driving Patterns Across Minnesota

Next, map your actual driving patterns across Minnesota for the next twelve months. Where do your vehicles operate daily? Minneapolis and St. Paul drivers face different theft and traffic risks than those operating primarily in suburban or rural areas. Document whether your team drives primarily on highways, urban streets, or a mix. A plumbing service making frequent short-distance residential calls has different accident frequency than a logistics company covering multiple counties. Your insurance cost depends heavily on these specifics, and vague descriptions lead to either overpaying for unnecessary coverage or discovering gaps when claims arise.

Compare Quotes from Multiple Carriers

Once you understand your fleet profile, compare quotes from multiple carriers through a licensed Minnesota agent who can access several insurers simultaneously. Commercial auto insurance for a light-duty vehicle typically costs $250 to $400 per month, but actual quotes for your specific fleet might range depending on vehicle types, driver records, and chosen limits. Request quotes with identical coverage parameters from at least three carriers so you’re comparing apples to apples. Ask each carrier about discounts specific to your situation: safety devices like GPS tracking reduce theft risk and lower premiums, while good driver records and completed defensive driving courses qualify for rate reductions. Some insurers offer bundling discounts if you carry general liability or property insurance with them, potentially saving 10 to 15 percent on your total premium.

Evaluate Financial Strength and Customer Support

Evaluate each quote’s financial strength ratings through A.M. Best or Standard & Poor’s, since the lowest price means nothing if the carrier struggles with claims payment. Request quotes with higher liability limits like $500,000 or $1,000,000 to see the actual cost difference, which often surprises business owners who discover that premium increases are modest compared to the protection gained. Finalize your choice based on three factors: does the coverage match your documented fleet and routes, do the financial ratings and customer reviews inspire confidence, and does the agent provide responsive support when you need policy adjustments or have questions?

Final Thoughts

Selecting the right Minnesota commercial auto coverage requires moving beyond state minimums and understanding your specific operational risks. Document your fleet composition and driving patterns with precision, compare quotes across multiple carriers to identify both cost differences and coverage variations, and prioritize financial strength ratings alongside premium pricing. Your vehicle types, routes, driver records, and claims history directly determine which coverage options matter most for your business.

Local insurance agents provide value that online quote tools cannot match-a Minnesota-based agent understands regional weather hazards, knows which carriers offer the best rates for your specific industry and location, and identifies coverage gaps that generic policies leave exposed. At Variant Insurance Group, we shop Minnesota’s top-rated insurance companies to find protection that matches your actual business operations rather than forcing you into standardized packages. We compare both protection and pricing, and we adjust your coverage as your business evolves.

Contact Variant Insurance Group to discuss your fleet, your routes, and your current coverage gaps. We’ll provide a customized quote that reflects your actual business needs and show you exactly what you’re paying for and why. Minnesota commercial auto coverage should protect your assets and your employees without forcing you to overpay for irrelevant protection.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation