Hosting on Airbnb can generate solid income, but it also exposes you to real financial risks. Property damage, liability claims, and income loss are genuine concerns that standard homeowners insurance typically won’t cover.

At Variant Insurance Group, we’ve seen too many Minnesota hosts operate without proper protection. The right Airbnb host insurance policy fills the gaps and gives you peace of mind while you grow your rental business.

What Airbnb Host Insurance Actually Covers

Airbnb’s Host Protection Insurance sounds comprehensive until you read the fine print. The platform offers Host Liability Insurance up to $1,000,000 for guest injuries and property damage, plus Host Damage Protection covering $3 million for property damage and lost income from cancellations. However, this coverage functions as a reimbursement program with strict conditions and third-party processing through Zurich, leaving significant gaps that expose Minnesota hosts to real financial risk. Airbnb explicitly excludes wear and tear, weather-related damage, mold, long-term liability, and intentional guest damage. You must report property damage claims within 14 days after checkout-late reporting results in denial regardless of documentation quality. This narrow window creates genuine risk, especially during busy seasons when administrative tasks pile up. Standard homeowners insurance compounds the problem further, actively excluding short-term rental activity and leaving you with no backup coverage when Airbnb’s program denies your claim.

Why Standalone Host Insurance Fills the Gaps

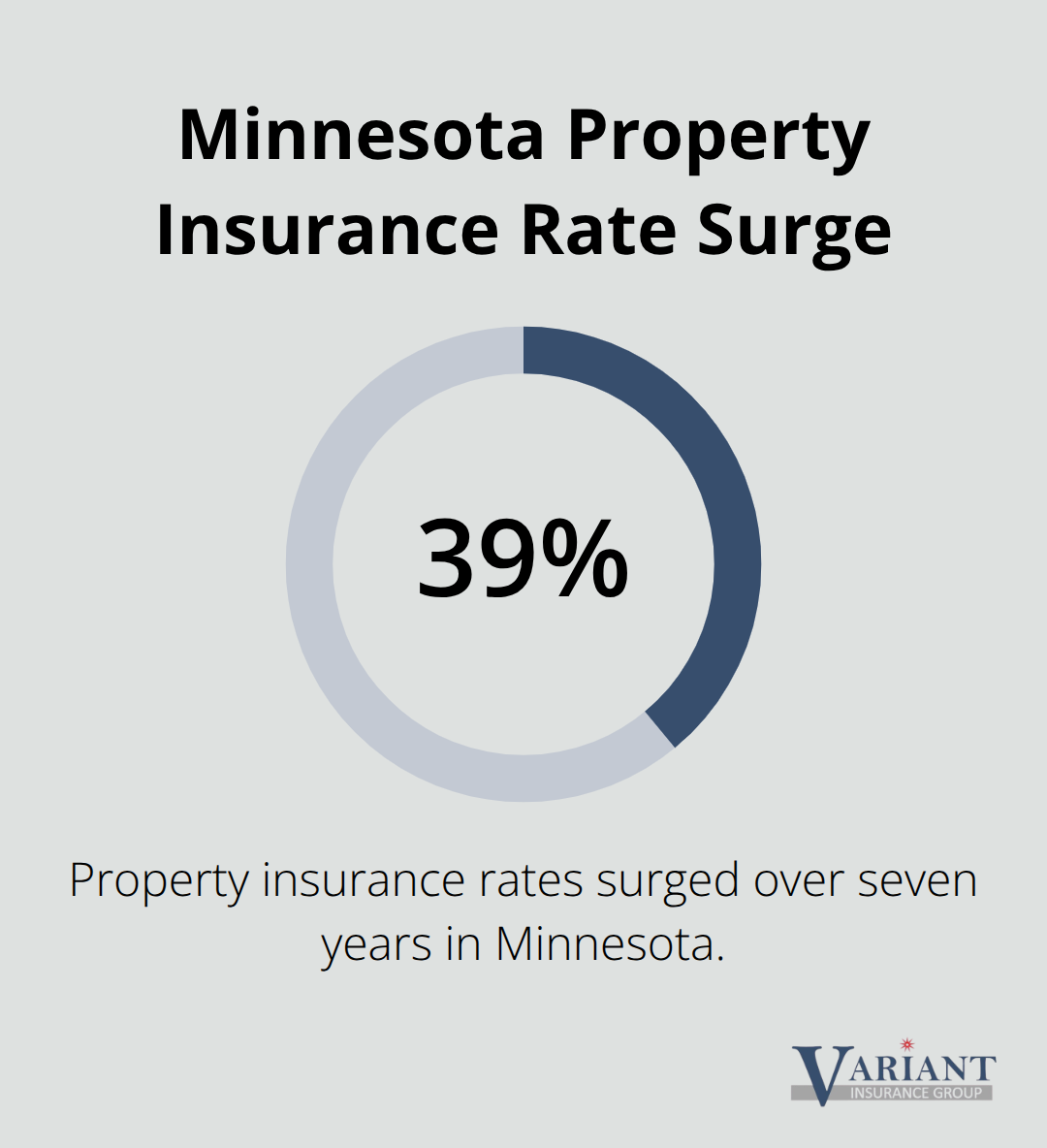

Dedicated short-term rental insurance addresses the realities of hosting paying guests and operates fundamentally differently from Airbnb’s protection program. These policies cover property damage from guests, comprehensive liability protection extending to off-premises activities like guided tours, and loss of rental income with no time limits-protecting your cash flow when a covered incident forces cancellation. Minnesota hosts face particular pressure from rising insurance costs. Property insurance rates surged 39% over seven years according to data from Capstone Insurance Group, and a single 2023 storm generated approximately $1 billion in insured losses across the Twin Cities and central Minnesota.

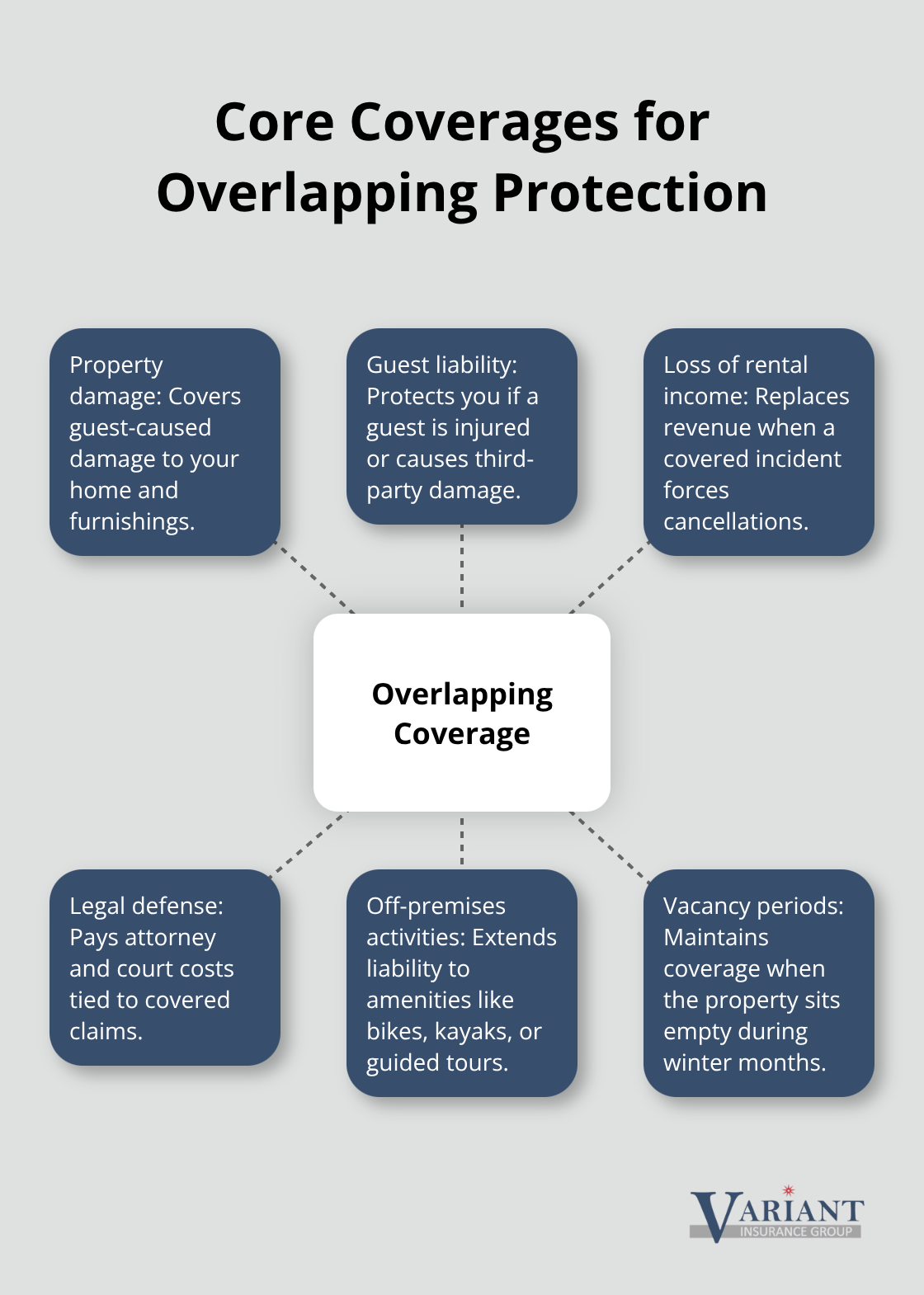

Standalone policies also include legal defense and cover scenarios Airbnb excludes, such as liability from guest-caused damage that falls outside their reimbursement rules. The premium difference between personal homeowners and host insurance reflects real risk; hosting strangers for money creates exposure that standard residential policies cannot address. Minnesota law increasingly requires proof of specific host insurance coverage, making standalone policies mandatory for legal compliance in many municipalities.

Building Your Complete Protection Strategy

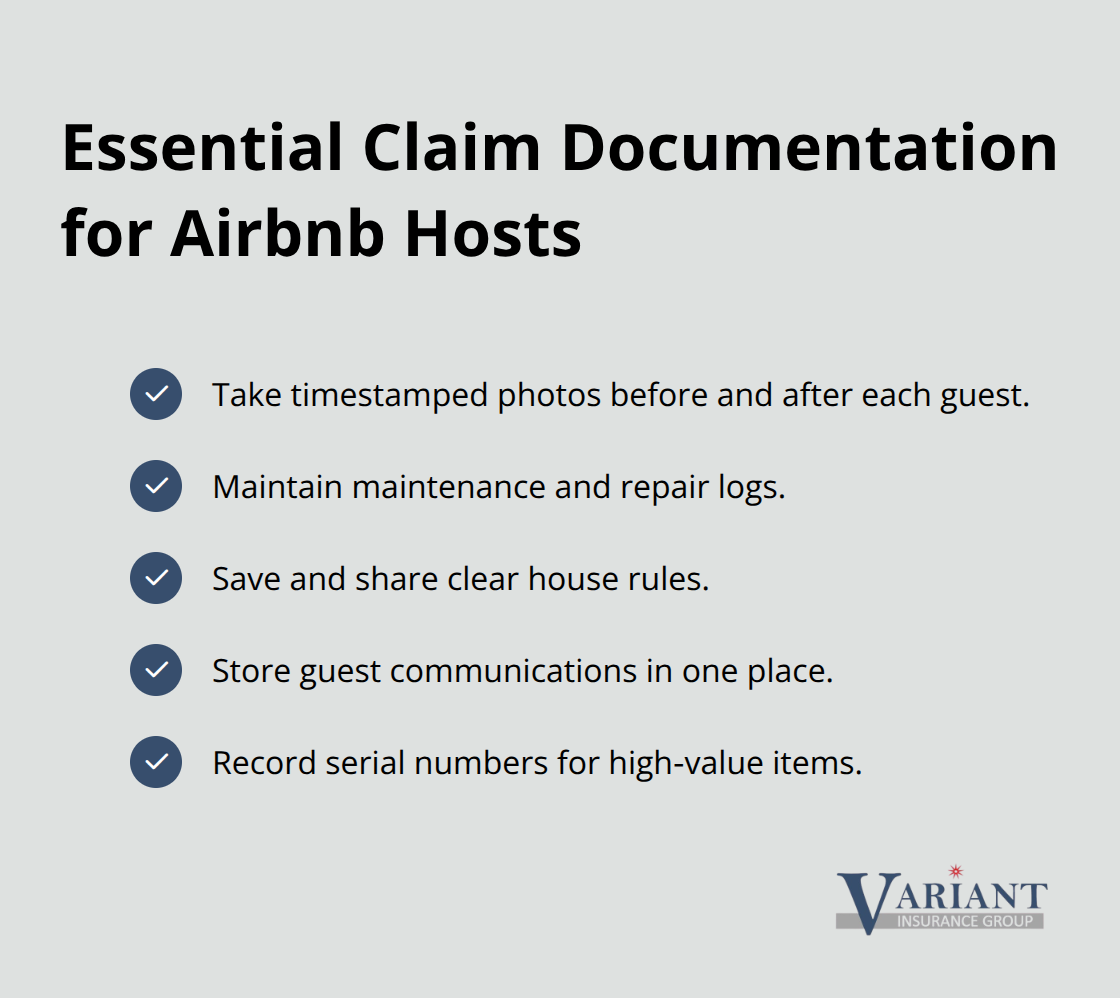

Relying solely on either Airbnb’s program or a standard homeowners policy creates dangerous blind spots in your financial protection. The most effective approach pairs Airbnb’s Host Protection Insurance with a dedicated short-term rental policy from a reputable provider, creating overlapping coverage that catches claims the platform denies. You need explicit coverage for property damage, guest liability, loss of rental income, and legal defense costs. High-value properties or those with amenities like pools, hot tubs, or off-premises equipment require additional evaluation to confirm adequate coverage limits. When shopping policies, verify that your chosen insurer explicitly covers short-term rentals and understand whether coverage applies during vacancy periods (which matters significantly for Minnesota’s seasonal hosting patterns). Document everything meticulously: timestamped photos before and after each guest, maintenance logs, house rules, and guest communications. This documentation becomes invaluable when filing claims, since insurers review evidence carefully before reimbursing claims.

Local insurance agents in Minnesota who understand the state’s climate risks and rental regulations can tailor coverage specifically for your property’s exposure rather than offering generic solutions designed for national markets.

What to Evaluate When Comparing Policies

Property value assessment forms the foundation of your coverage decision. Calculate your home’s replacement cost, furnishings value, and potential income loss during peak seasons to determine appropriate coverage limits. Compare deductibles across policies-higher deductibles lower premiums but increase your out-of-pocket costs when claims occur. Review what each policy excludes and identify which gaps matter most for your specific property and hosting model. Some policies exclude certain guest activities or amenities, while others limit coverage during extended vacancy periods. Verify whether the insurer covers your property type (single-family home, condo, multi-unit building) and whether they impose occupancy restrictions that conflict with your hosting schedule. Request quotes from multiple providers to understand pricing variations and coverage differences. An independent insurance agent can help you navigate these comparisons and identify which policy aligns with your actual risk exposure and financial situation.

Coverage Options for Minnesota Airbnb Hosts

What Airbnb’s Built-In Protection Actually Covers

Airbnb’s Host Liability Insurance covers guest injuries and property damage up to $1,000,000, while Host Damage Protection extends to $3,000,000 for property damage and lost income from cancellations. However, Zurich processes these claims as a reimbursement program with strict timelines and exclusions that expose Minnesota hosts to significant risk. You must report property damage within 14 days of checkout or face automatic denial. Wear and tear, weather damage, mold, and intentional guest misconduct fall outside coverage entirely. A single storm in 2023 generated approximately $1 billion in insured losses across the Twin Cities and central Minnesota, demonstrating how quickly weather events can exceed what Airbnb’s program covers.

Many Minnesota municipalities now require proof of specific host insurance before allowing short-term rentals, making Airbnb’s coverage legally insufficient on its own. The platform’s reimbursement structure also means you pay out-of-pocket first and wait for Zurich to approve repayment, creating cash flow problems during peak hosting seasons when you need income most.

Why Standalone Host Insurance Addresses Real Gaps

Third-party host insurance policies address these limitations directly by covering high-turnover rental operations rather than occasional residential use. These standalone policies typically include property damage from guests, comprehensive liability extending to off-premises amenities like kayaks or bikes, loss of rental income with no time restrictions, and legal defense costs. Coverage applies during vacancy periods, which matters significantly for Minnesota’s seasonal hosting patterns where properties sit empty during winter months.

Premium costs reflect actual risk; you pay more than standard homeowners insurance because you protect income-generating activity. High-value properties or those with pools, hot tubs, or detached structures require additional evaluation to confirm replacement cost coverage and adequate liability limits. Amenities liability coverage protects you when guests take property off-site and cause damage or injury.

Evaluating Policy Exclusions and Your Hosting Model

Some policies exclude certain activities or guest types, so you must verify that coverage aligns with your specific hosting model before purchasing. A policy that works for a basic single-family home may not protect a property with a hot tub, sauna, or guided experience offerings. Review whether the insurer covers your property type (single-family home, condo, multi-unit building) and whether they impose occupancy restrictions that conflict with your hosting schedule.

Request quotes from multiple providers to understand pricing variations and coverage differences. An independent insurance agent familiar with Minnesota’s climate risks and rental regulations can help you navigate these comparisons and identify which policy aligns with your actual risk exposure.

Building Overlapping Protection

Pairing Airbnb’s Host Protection Insurance with a dedicated host policy creates overlapping protection that catches claims one program denies, ensuring your income and property remain protected regardless of which insurer processes the claim. This dual-coverage approach transforms your financial security from a single point of failure into a resilient system.

When you face a claim denial from Airbnb’s reimbursement program, your standalone policy steps in to cover the gap. This strategy proves especially valuable for Minnesota hosts who experience seasonal income fluctuations and cannot afford unexpected out-of-pocket losses.

The right combination of coverage transforms hosting from a financially precarious venture into a sustainable business model. Understanding which gaps exist in Airbnb’s program and how standalone policies fill those gaps positions you to make informed decisions about your protection strategy. As you evaluate specific policies and providers, the next step involves assessing your property’s unique characteristics and determining the coverage limits that match your actual exposure.

Selecting the Right Policy for Your Minnesota Property

Calculate your property’s true replacement cost

Choosing an Airbnb host insurance policy requires honest assessment of your property’s actual value and the income you depend on. Start by calculating replacement cost for your home, furnishings, and appliances separately-this number drives your coverage limits and directly impacts your premium. Many Minnesota hosts underestimate replacement costs because they think in terms of what they paid rather than what it would cost to rebuild today. A 2023 storm generated approximately $1 billion in insured losses across the Twin Cities and central Minnesota, demonstrating how quickly property damage can exceed expectations and making accurate valuation critical.

Document your property’s condition with timestamped photos of every room, major appliances, and furnishings before you start hosting. This documentation becomes invaluable when discussing coverage limits with insurers and when filing claims. Take photos from multiple angles and capture serial numbers on high-value items to establish proof of ownership and condition.

Assess Your Income Protection Needs

Calculate your average monthly rental income during peak season and identify how many days of lost income would create financial hardship. If you depend on Airbnb income to cover your mortgage, loss-of-income coverage becomes non-negotiable rather than optional. A policy with inadequate loss-of-income limits forces you to absorb cancellation costs yourself during the months when you need revenue most.

Review whether the policy covers your property during vacancy periods-this matters significantly when your home sits empty during winter months. Minnesota’s seasonal hosting patterns create extended gaps in occupancy that standard policies may not address, leaving you exposed during the months when you cannot generate income.

Compare Deductibles and Coverage Limits

Comparing deductibles across policies reveals how much you’ll actually pay when claims occur. A policy with a $500 deductible and $1,200 annual premium looks cheaper than one with a $1,000 deductible and $900 annual premium until you file a claim and realize the difference in your out-of-pocket costs. Request quotes from multiple providers and examine what each policy explicitly excludes for your property type and hosting model.

Some insurers impose occupancy restrictions that conflict with seasonal hosting patterns common in Minnesota, while others exclude coverage for pools, hot tubs, or guest amenities entirely. Verify that the policy covers your property type (single-family home, condo, multi-unit building) and that coverage aligns with your specific hosting schedule and activities.

Work With Local Insurance Expertise

An independent insurance agent familiar with Minnesota’s climate risks and local rental regulations can help you navigate these comparisons and identify which policy aligns with your actual risk exposure rather than offering generic solutions. Local agents understand how winter weather, seasonal vacancy patterns, and municipal regulations affect your coverage needs in ways that national insurers often miss.

At Variant Insurance Group, we shop Minnesota’s top-rated insurance companies to find host policies that match your specific property characteristics and income requirements, ensuring you get the coverage you actually need at pricing that fits your business model.

Final Thoughts

Airbnb host insurance protects your income and property from real financial risks that come with hosting paying guests. Airbnb’s built-in coverage sounds comprehensive until you encounter its strict timelines, exclusions, and reimbursement delays, while standard homeowners insurance actively excludes short-term rental activity and leaves you with no backup protection. The solution pairs Airbnb’s Host Protection Insurance with a dedicated host policy that covers property damage, guest liability, loss of rental income, and legal defense costs.

Minnesota hosts face particular pressure from rising insurance costs and increasingly strict municipal regulations that require proof of specific host insurance coverage. A single 2023 storm generated approximately $1 billion in insured losses across the Twin Cities and central Minnesota, demonstrating how quickly weather events exceed what basic coverage provides. Property insurance rates surged 39% over seven years, making it essential to shop strategically rather than accept the first quote you receive.

Start by calculating your property’s true replacement cost, including furnishings and appliances, then assess how many days of lost income would create financial hardship. Request quotes from multiple providers and compare deductibles, coverage limits, and exclusions carefully-verify that any policy you consider explicitly covers short-term rentals and addresses your specific property type and hosting model. Contact Variant Insurance Group to discuss your Airbnb host insurance coverage needs with professionals who understand Minnesota’s unique hosting environment and can help you build protection that actually works for your business.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation