Personal umbrella insurance provides extra liability protection beyond your standard auto and homeowners policies. This coverage kicks in when your primary insurance limits are exhausted, protecting your assets from major lawsuits.

We at Variant Insurance Group see many Minnesota residents asking what is personal umbrella insurance and whether they need it. The answer depends on your assets, lifestyle, and potential liability risks.

How Does Umbrella Insurance Work

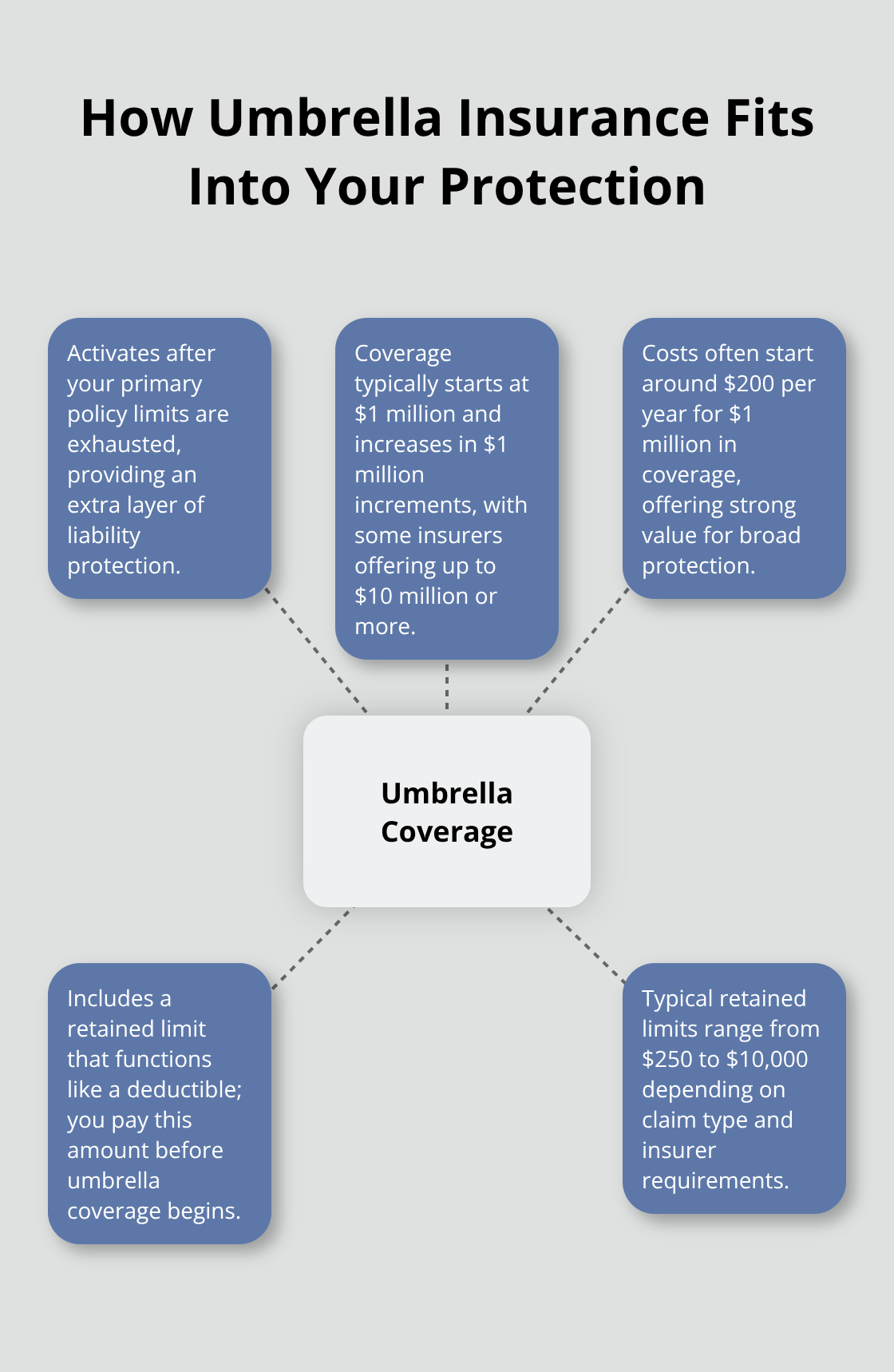

Personal umbrella insurance acts as a secondary layer of protection that activates when your primary insurance policies reach their limits. In Minnesota, most insurers require minimum liability limits of $250,000 for auto insurance and $300,000 for homeowners insurance before you qualify for umbrella coverage. When a claim exceeds these primary limits, your umbrella policy steps in to cover the costs up to your selected coverage amount.

Coverage Structure and Limits

Umbrella policies typically start at $1 million in coverage and increase in $1 million increments, with some insurers offering up to $10 million or more. According to the Insurance Information Institute, the cost typically starts around $200 per year for $1 million of coverage, which makes it remarkably affordable protection. The policy includes a retained limit (similar to a deductible), which you pay before umbrella coverage begins. This retained limit usually ranges from $250 to $10,000, depending on the type of claim and your insurer’s requirements.

What Umbrella Insurance Covers

Your umbrella policy protects against liability claims that standard policies often exclude, including defamation, libel, slander, and false imprisonment. It covers legal defense costs even for frivolous lawsuits, which can easily reach six figures. The policy also extends to incidents that involve rental properties, volunteer work, and global travel. Most importantly, umbrella insurance protects your savings accounts, investment portfolios, real estate, and future income from seizure to satisfy large judgments against you.

How Claims Work in Practice

When someone files a lawsuit against you, your primary insurance handles the claim first. If the judgment or settlement exceeds your primary policy limits, the umbrella policy pays the excess amount (minus your retained limit). This seamless process protects you from personal financial responsibility for catastrophic claims that could otherwise devastate your financial future.

Now that you understand how umbrella insurance functions, the next question becomes whether you actually need this additional protection.

Who Needs Umbrella Insurance

Minnesota residents with assets exceeding $500,000 should seriously consider umbrella insurance, but the need extends far beyond high net worth individuals. Civil case filings in U.S. district courts have increased significantly, making liability exposure a real risk for anyone with modest savings or property. Homeowners with teenage drivers face particularly high risks, as young drivers are involved in accidents at rates three times higher than experienced drivers. Property owners, landlords, and anyone who hosts gatherings create additional liability exposure that standard policies may not adequately cover.

High-Risk Activities That Demand Coverage

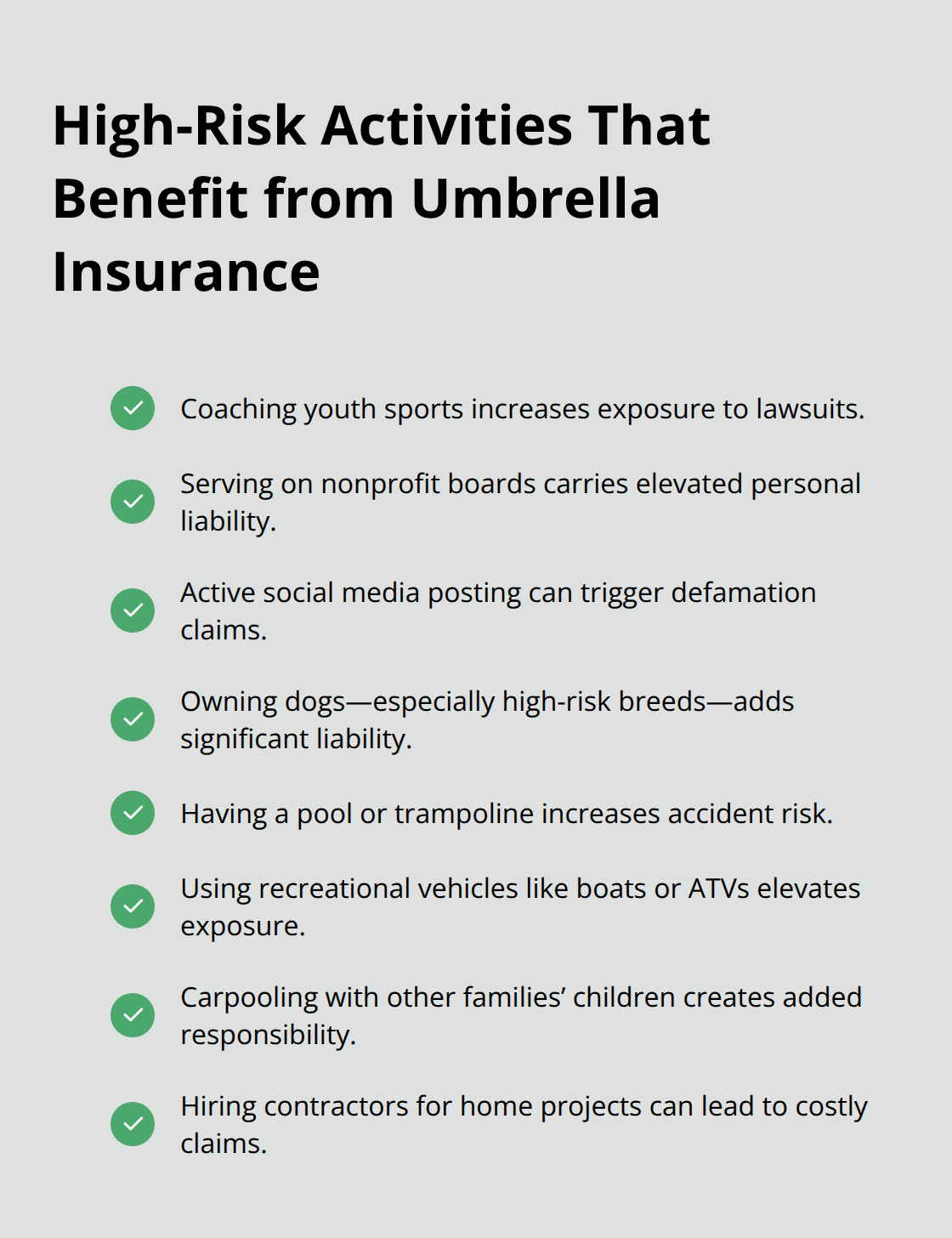

Coaches of youth sports, nonprofit board members, and active social media users face significantly increased lawsuit risk. Dog owners face substantial liability, especially with breeds that insurance companies classify as high-risk. Pool owners, trampoline owners, and those with recreational vehicles like boats or ATVs should view umbrella insurance as non-negotiable protection. Even seemingly innocent activities like carpools with other families’ children or home projects with contractors can expose you to million-dollar lawsuits if accidents occur.

Professional and Online Liability Risks

Professionals in healthcare, real estate, consulting, or any client-facing role face elevated lawsuit risks that require umbrella protection. Social media users who post product reviews, share opinions, or engage in online discussions risk defamation claims that can cost hundreds of thousands in legal fees alone. The rise of litigation funding has made it easier for attorneys to pursue high-value claims (targeting higher available limits through improved identification methods), which makes umbrella insurance more important than ever.

Asset Protection Beyond Net Worth

Your future income streams need protection just as much as your current assets. Courts can garnish wages for decades to satisfy large judgments, which means even young professionals with modest current assets face significant financial risk. Retirees with valuable properties or those who engage in risky hobbies particularly benefit from umbrella coverage (especially given their fixed incomes and limited ability to recover from financial setbacks).

The comprehensive protection umbrella insurance provides extends well beyond simple asset protection, offering benefits that can safeguard your entire financial future.

What Protection Does Umbrella Insurance Actually Provide

Financial Shield Against Catastrophic Judgments

Umbrella insurance protects your assets when lawsuits exceed your primary policy limits, which happens more frequently than most people realize. The Insurance Information Institute reports that the average umbrella policy combined ratio reached 200% in 2024, which means claims costs doubled premium income, largely due to attorneys who target higher available limits through improved identification methods. A single car accident that results in permanent disability can generate judgments that exceed $3 million, while defamation claims from social media posts average $200,000 in legal costs alone. Without umbrella coverage, courts can seize your savings accounts, investment portfolios, real estate equity, and garnish your wages for decades to satisfy these judgments.

Legal Defense Cost Coverage That Saves Fortunes

Legal defense costs often exceed actual damage awards, which makes this benefit extremely valuable. Umbrella policies cover attorney fees, court costs, and expert witness expenses even for frivolous lawsuits that you ultimately win. A typical defamation case costs $150,000 to defend regardless of the outcome, while personal injury lawsuits average $75,000 in legal fees before they reach trial. The Wall Street Journal highlighted concerns about increased umbrella claims that lead to premium hikes, but the alternative of paying these costs out-of-pocket would devastate most families financially. Your umbrella policy pays these expenses above your retained limit (which protects your assets from depletion during lengthy legal proceedings).

Long-Term Financial Security Protection

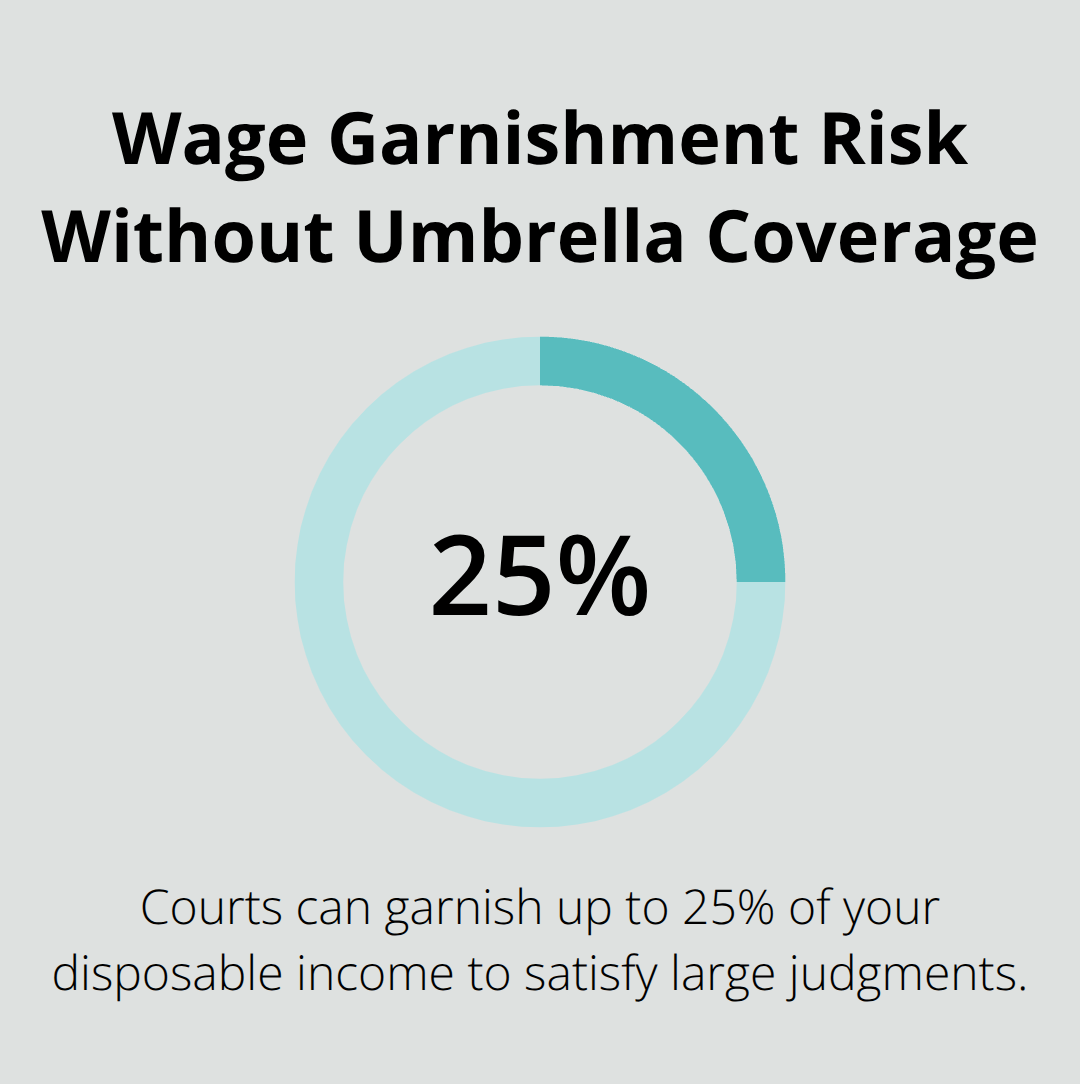

Umbrella insurance protects your future earning capacity, not just current assets. Courts can garnish up to 25% of your disposable income for decades to satisfy large judgments, which means even young professionals with modest current assets face substantial risk. The U.S. Personal Umbrella market generates $6.6 billion in premiums annually and constitutes less than 1% of the Property & Casualty market, yet provides protection that no other insurance product can match.

This coverage protects retirement savings, children’s education funds, and your ability to maintain your standard of living after a catastrophic liability claim (which makes it an essential component of comprehensive financial planning).

Final Thoughts

Personal umbrella insurance provides financial protection that standard policies cannot match. The coverage shields your assets from catastrophic lawsuits, pays legal defense costs that often exceed damage awards, and protects your future income from wage garnishment. With civil litigation on the rise and attorneys who target higher policy limits, Minnesota residents with assets to protect must understand what is personal umbrella insurance.

Your liability exposure extends beyond your net worth. Everyday activities like driving, hosting gatherings, or posting on social media create risks that could result in million-dollar judgments. The cost of umbrella coverage starts around $200 annually for $1 million in protection (making it one of the most cost-effective insurance investments available).

We at Variant Insurance Group help Minnesota residents assess their liability risks and find appropriate umbrella coverage. Our team shops multiple top-rated insurance companies to find the best protection for your specific situation. Contact us today to review your current coverage and protect your financial future with comprehensive umbrella insurance.