Hosting on Airbnb comes with real financial exposure. Guest damage, liability claims, and lost income can quickly drain your profits if you’re not properly protected.

At Variant Insurance Group, we’ve seen Minnesota hosts face thousands in unexpected costs because standard homeowners policies don’t cover short-term rentals. Airbnb’s guest property coverage has significant gaps that leave your business vulnerable.

This guide walks you through the coverage options that actually protect your Airbnb business.

Why Airbnb’s Built-In Protection Isn’t Enough

The Limits of Airbnb’s Host Protection Program

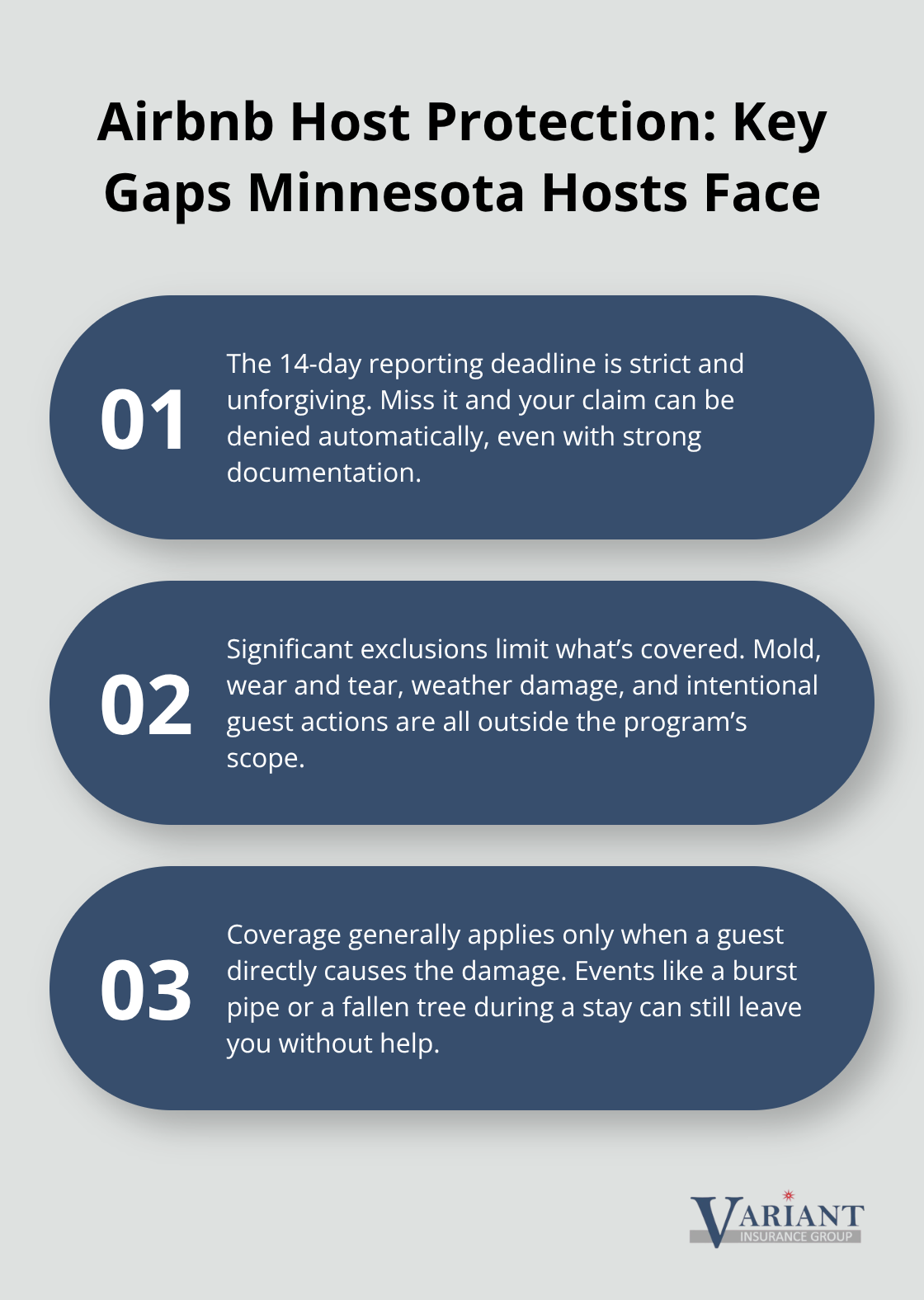

Airbnb provides host protection coverage that sounds comprehensive on the surface. The platform offers up to $3 million in property damage reimbursement and $1 million in liability coverage at no extra cost. However, this protection has strict limitations that create serious gaps for Minnesota hosts. The 14-day reporting deadline is unforgiving-file late and your claim gets automatically denied, regardless of documentation quality. Airbnb explicitly excludes mold, wear and tear, weather damage, and intentional guest actions.

More critically, the program only covers damage when a guest is directly responsible. If a pipe bursts during a guest’s stay or a tree falls on your roof, Airbnb’s coverage won’t help.

The reimbursement process moves slowly through Airbnb Support or, in Washington state, through an insurance company, leaving you without income while repairs happen. Property damage claims require photos, repair estimates, and receipts-all within that tight 14-day window. Many Minnesota hosts discover too late that Airbnb’s protection doesn’t cover loss of rental income when they need to cancel bookings due to repairs, doesn’t apply to vehicles or boats stored on the property in all situations, and excludes damage from natural disasters like the $1 billion in insured losses Minnesota experienced from the 2023 storms across the Twin Cities and central Minnesota.

Why Standard Homeowners Insurance Fails

Standard homeowners insurance makes the situation worse. Most policies explicitly exclude short-term rental activity, leaving you with zero coverage for guest-caused damage, liability claims from guests, or lost income. Many Minnesota municipalities now require proof of specific host insurance before allowing short-term rentals, making dedicated coverage not just smart but legally necessary. The financial stakes are real-one guest causes $8,000 in damage, a liability lawsuit from a guest injury, or lost bookings during repairs can wipe out months of profit. Hosts operating without proper coverage face the choice between absorbing these costs personally or discovering their homeowners policy won’t pay.

The Solution: Overlapping Coverage

Dedicated short-term rental insurance fills these gaps by covering what Airbnb doesn’t, including property damage with no sub-limits, liability protection up to $2 million, and business revenue protection that pays actual losses sustained during claim periods. The combination of Airbnb’s built-in protection paired with dedicated short-term rental insurance creates overlapping coverage that catches claims the platform denies. This layered approach protects your Minnesota property from the specific risks that standard policies ignore. When you pair platform protection with specialized coverage, you eliminate the financial exposure that catches most hosts unprepared. Understanding what each policy covers-and what it doesn’t-determines whether a single claim destroys your business or simply triggers your insurance. The next section walks you through the specific types of coverage available and how they work together to protect your Airbnb operation.

Coverage That Actually Protects Your Minnesota Airbnb

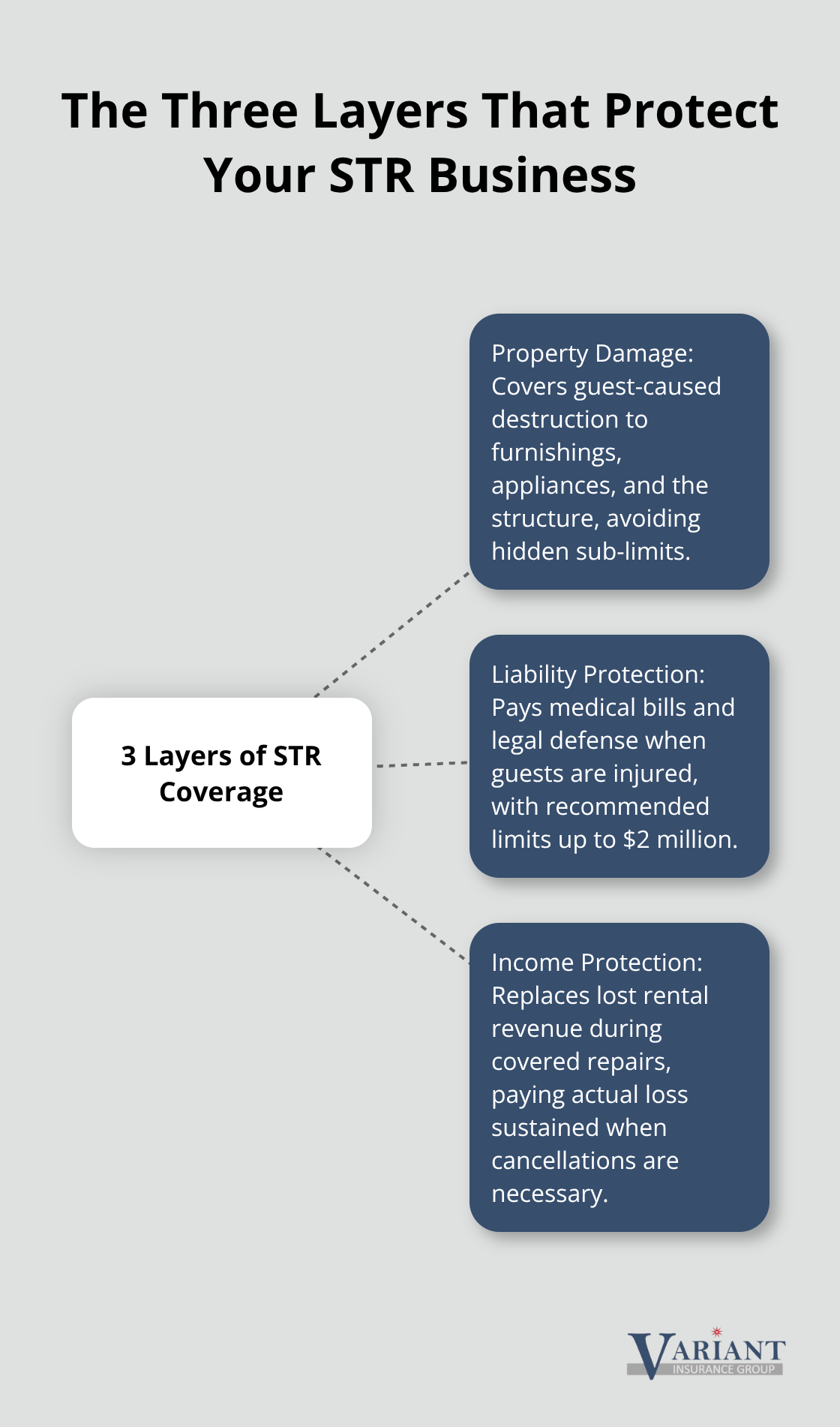

Short-term rental insurance comes in three distinct layers, and Minnesota hosts need all three working together to stay protected. Property damage coverage handles what happens when guests destroy your furnishings, appliances, or the structure itself. Liability protection covers medical bills and legal costs when a guest gets injured on your property. Income protection replaces lost rental revenue when damage forces you to cancel bookings. Most hosts focus only on property damage and ignore the other two, which costs thousands when a guest breaks a leg on your deck or a backed-up sewer line shuts down bookings for two weeks.

Why Replacement Cost Matters More Than You Think

The key difference between adequate protection and financial disaster often comes down to whether your policy covers actual cash value or replacement cost. Replacement cost valuation means your insurer pays what it costs to replace damaged items today, not what they were worth five years ago when you bought them. A guest spills wine on your $3,000 sectional sofa, and replacement cost coverage pays $3,000 to replace it. Actual cash value would pay $1,500 after depreciation, leaving you $1,500 short. Specialized carriers use replacement cost for both building and contents, which is the only approach that makes financial sense for active rental properties. Airbnb’s reimbursement program operates differently and moves slowly through their claims process, often taking weeks to determine what they’ll actually pay.

Property Damage Coverage Without Hidden Limits

Property damage coverage needs to address guest-caused destruction specifically, not lump it together with vandalism or wear and tear exclusions that standard policies use. You need a policy that doesn’t artificially restrict payouts for guest destruction beyond your overall policy limit. This matters because guest damage claims frequently exceed $5,000, and you require protection that covers the full amount. Dedicated short-term rental policies combine all three coverage types, while Airbnb’s built-in coverage leaves significant gaps in each category.

Liability Protection: The Minimum You Need

Liability coverage starting at $1 million per occurrence is the minimum for Minnesota hosts, though upgrading to $2 million is strongly recommended to guard against serious guest-injury lawsuits. A guest falls down your stairs and suffers a broken hip requiring surgery and physical therapy, and suddenly you face $50,000 to $150,000 in medical costs plus potential pain-and-suffering damages. Your $1 million liability limit covers the claim, but barely. Off-premises liability protection extends coverage to amenities like bicycles, kayaks, or hot tubs that guests use away from your main property, addressing exposure most hosts overlook.

Income Protection: The Coverage Most Hosts Miss

Income protection is where most hosts remain dangerously exposed because they don’t realize Airbnb’s coverage excludes lost rental revenue in many situations. Dedicated STR policies pay actual loss sustained if a covered claim prevents you from renting, with no time limit on how long you collect payments. If a guest causes $8,000 in water damage and repairs take 30 days during peak summer season when you’d normally book at $200 per night, your income protection pays $6,000 in lost revenue. Airbnb might reimburse the repair costs but not the lost income, leaving that gap for your dedicated policy to fill. This three-layer approach-property, liability, and income-transforms how you handle the financial impact of guest-related incidents. The next section examines how to select a policy that actually matches your property’s specific risks and your hosting volume.

Selecting the Right Coverage for Your Minnesota Property

Calculate Your Actual Replacement Costs

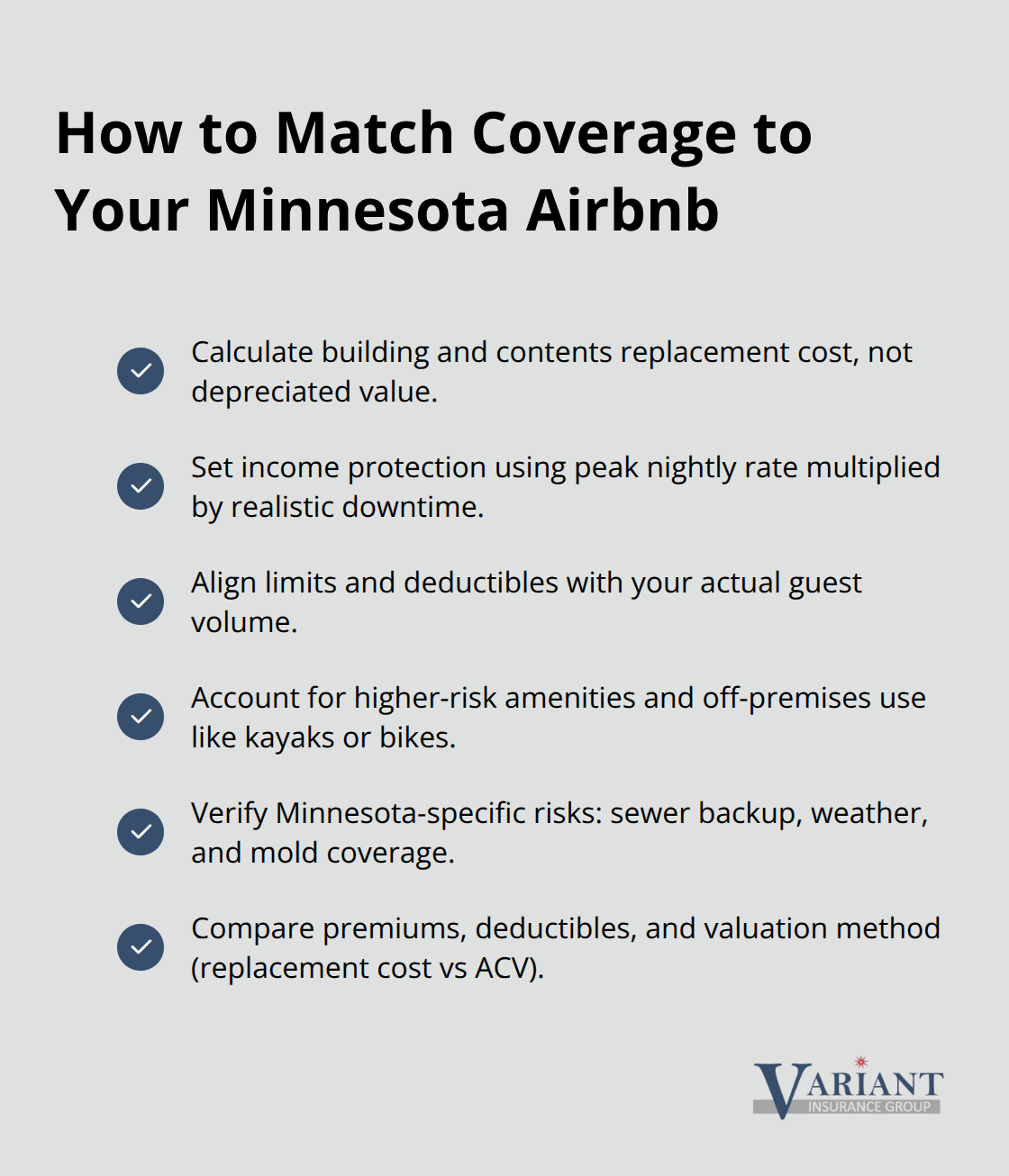

Choosing an Airbnb host insurance policy requires matching coverage to your specific property, guest patterns, and financial exposure rather than picking the cheapest option available. Start by calculating your actual replacement cost for the building, furnishings, and equipment. If your Minnesota home is worth $400,000 and you’ve furnished it with $50,000 in rental-specific items, you need property coverage that reflects those numbers, not a generic amount. Next, determine your peak-season daily rate and multiply it by how many days of lost income would create serious financial hardship. A host earning $200 per night during summer months needs income protection that covers at least 30 days of lost revenue, roughly $6,000, to survive an extended repair period.

Match Coverage to Your Guest Volume and Amenities

Guest volume matters significantly because high-turnover properties face greater exposure to damage claims, theft, and liability incidents. A property with 40 bookings annually faces different risk than one with 100 bookings, and your coverage should reflect that difference. Document your property’s amenities too because a home with a pool, hot tub, or available off-site equipment like kayaks or bicycles increases liability exposure substantially. These specific details determine whether a standard coverage package protects you adequately or leaves dangerous gaps when a claim occurs.

Look Beyond Premium Price to Actual Protection

Comparing policies requires looking beyond premium price to understand what you’re actually buying. A policy costing $900 annually with a $2,500 deductible and replacement cost valuation might cost less than one priced at $1,200 with a $500 deductible and actual cash value coverage, but the cheaper option leaves you exposed. When a $4,000 guest-damage claim occurs, the $900 policy makes you cover the first $2,500 out of pocket, then reimburses only depreciated value on the remaining amount. The $1,200 policy covers replacement cost with a smaller deductible, potentially saving you $3,000 on a single claim.

Verify Coverage for Minnesota-Specific Risks

Review whether policies exclude specific risks Minnesota hosts encounter regularly, particularly weather-related damage, mold coverage, and sewer backup protection. Many standard policies exclude sewer and drain backup entirely, yet a backed-up sewer line during a guest stay creates both repair costs and lost income. Verify that guest-caused damage receives treatment separate from vandalism or wear-and-tear exclusions, ensuring full coverage for intentional or accidental guest destruction. Check whether the policy covers your property during vacancy periods since Minnesota’s seasonal hosting patterns often include gaps between summer and fall bookings when properties sit empty but remain exposed.

Confirm Off-Premises Liability Protection

Finally, confirm that liability coverage extends to off-premises guest activities, not just incidents on your property. A guest borrows your kayak, gets injured, and sues for $75,000 in medical costs. Without off-premises liability protection, you’re personally responsible for amounts exceeding your on-property coverage limits.

Final Thoughts

Protecting your Minnesota Airbnb requires moving beyond what the platform provides. Airbnb’s built-in coverage sounds comprehensive until you file a claim and discover the 14-day deadline, exclusions for weather damage, and gaps in income protection. Standard homeowners insurance won’t help because it explicitly excludes short-term rental activity, leaving you personally responsible for guest-caused losses that a dedicated policy would cover.

The solution pairs Airbnb’s host protection with dedicated short-term rental insurance that covers property damage with replacement cost valuation, liability protection up to $2 million, and business revenue that pays actual losses sustained during claim periods. This layered approach catches claims the platform denies and protects your income when damage forces cancellations. Calculate your replacement costs, match coverage to your guest volume and amenities, and verify that policies address Minnesota-specific risks like sewer backup and weather exposure.

At Variant Insurance Group, we help Minnesota hosts build the Airbnb guests property coverage strategy that actually protects your business. Our team understands the gaps in platform protection and shops Minnesota’s top-rated insurance companies to match you with policies designed specifically for vacation rentals. Contact us to review your current protection and secure the comprehensive coverage your Minnesota Airbnb deserves.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation