Construction contractor risk management isn’t optional in Minnesota-it’s the foundation of a sustainable business. Weather, accidents, and equipment losses threaten projects every season, and the costs add up fast.

At Variant Insurance Group, we’ve worked with contractors across the state who’ve learned this lesson the hard way. The right coverage and smart practices protect both your team and your bottom line.

What Makes Minnesota Construction So Risky

Weather Creates Predictable but Costly Disruptions

Minnesota’s construction environment presents hazards that contractors cannot ignore. Winter weather alone costs the state’s construction industry millions annually-ice, snow, and sub-zero temperatures shut down projects, damage equipment, and force costly delays. According to the National Weather Service, Minnesota experiences an average of 40 inches of snow per year, with many regions receiving significantly more. Spring thaw brings flooding risks that compromise foundations and site access. Summer thunderstorms knock over cranes and scaffolding. Fall’s unpredictable temperature swings crack freshly poured concrete. These aren’t rare events; they’re predictable seasonal patterns that affect every Minnesota contractor’s schedule and budget.

On-Site Injuries Drive the Highest Costs

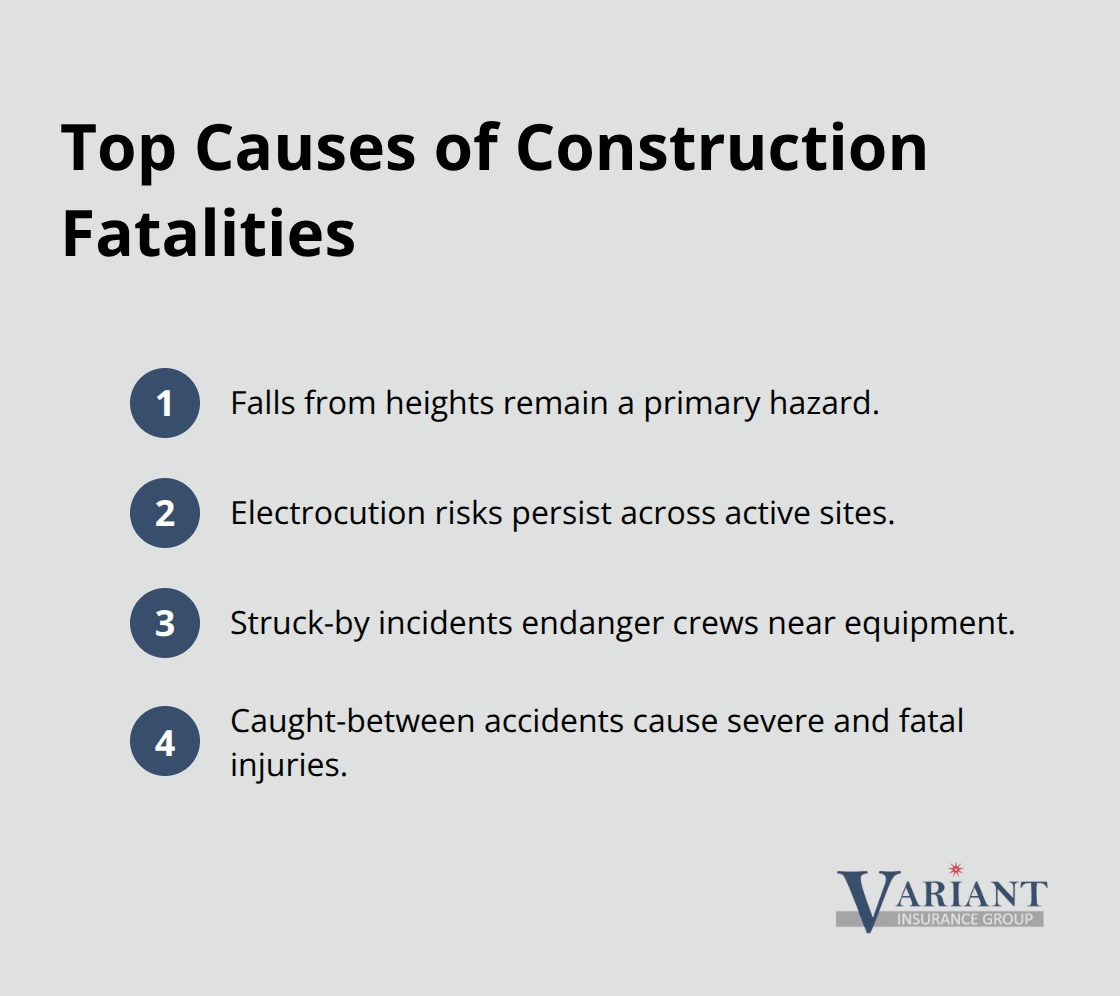

On-site injuries compound weather challenges and represent the most expensive risk contractors face. MNOSHA, Minnesota’s state occupational safety authority, tracks construction injuries across the state, and the data is sobering. Falls from heights, electrocution, struck-by incidents, and caught-between accidents remain the leading causes of construction fatalities nationwide and in Minnesota specifically. A single serious injury costs between $40,000 and $1 million in direct and indirect expenses, depending on severity.

These figures don’t account for lost productivity, reduced morale, or the emotional toll on your team.

Equipment Theft and Damage Erode Profitability

Equipment theft and damage drain contractor profitability faster than most realize. Construction sites lose approximately $1 billion in tools and equipment annually across the United States, with Minnesota’s urban and suburban job sites particularly vulnerable. Copper theft from HVAC systems, diesel fuel siphoning, and tool disappearance happen on nearly every multi-week project. Equipment damage from weather, improper operation, or maintenance neglect accelerates depreciation and forces expensive repairs that weren’t budgeted. A single excavator breakdown idles an entire crew for days, costing $2,000 to $5,000 per day in lost productivity alone.

Why These Risks Demand Immediate Action

Contractors who treat these risks as inevitable rather than manageable watch their margins evaporate and their insurance premiums climb year after year. The financial impact extends beyond immediate losses-repeated claims, safety violations, and equipment damage create a cycle that compounds over time. Understanding what coverage protects your business and which practices prevent losses separates contractors who thrive from those who struggle.

Essential Insurance Coverage for Minnesota Contractors

General Liability Protection Reflects Your Project Reality

General liability insurance protects contractors when property damage or bodily injury claims arise on job sites, and Minnesota contractors need coverage limits that reflect actual project costs, not insurance industry minimums. A $1 million general liability policy sounds substantial until you realize that a single incident causing structural damage to a client’s building or severe injury to a worker can exceed that amount in litigation costs alone. Contractors should evaluate their typical project values and contract requirements before selecting limits. Many Minnesota general contractors carry $2 million in general liability coverage, which aligns with contract demands from developers and property owners across the state.

Your policy should also include contractual liability coverage, which protects you when you’ve agreed to hold clients harmless in construction contracts-a standard requirement on commercial projects in Minnesota.

Workers Compensation: State Requirement and Financial Incentive

Workers compensation coverage is not optional in Minnesota; state law requires it for any contractor with employees, and MNOSHA enforces compliance through inspections and penalties. The cost varies based on your payroll, job classification, and safety record, but a contractor with a strong safety program and no claims history pays substantially less than one with repeated incidents.

Minnesota’s workers compensation system is state-administered and self-insured, meaning claims go through a defined system with predictable timelines and benefits. Experience modification rates, calculated annually by the state, directly impact premiums-contractors with injury histories pay 25 to 50 percent more than those with clean records. This creates a financial incentive to invest in genuine safety improvements, not just paperwork compliance.

Commercial Auto and Equipment Coverage Close Critical Gaps

Commercial auto insurance covers vehicles used for construction work, and Minnesota contractors often underestimate their exposure here. A crew member driving a company truck to a supplier and causing an accident creates liability that extends beyond the vehicle itself. Contractors who carry only minimum state liability limits on commercial vehicles face uncovered damages when incidents occur.

Equipment insurance protects tools, machinery, and materials on job sites from theft, weather damage, and operational damage. Many contractors assume their general liability policy covers equipment, but it does not. A $50,000 investment in tools and equipment left unattended on a multi-week project needs dedicated coverage, particularly in Minnesota’s urban areas where theft rates run higher than national averages.

Inland marine coverage insures equipment in transit and at job sites, and it protects excavators, compressors, and portable generators that move between projects. Contractors who’ve experienced equipment theft or weather damage report that the cost of replacement or repair-combined with project delays-often exceeds the equipment’s original value.

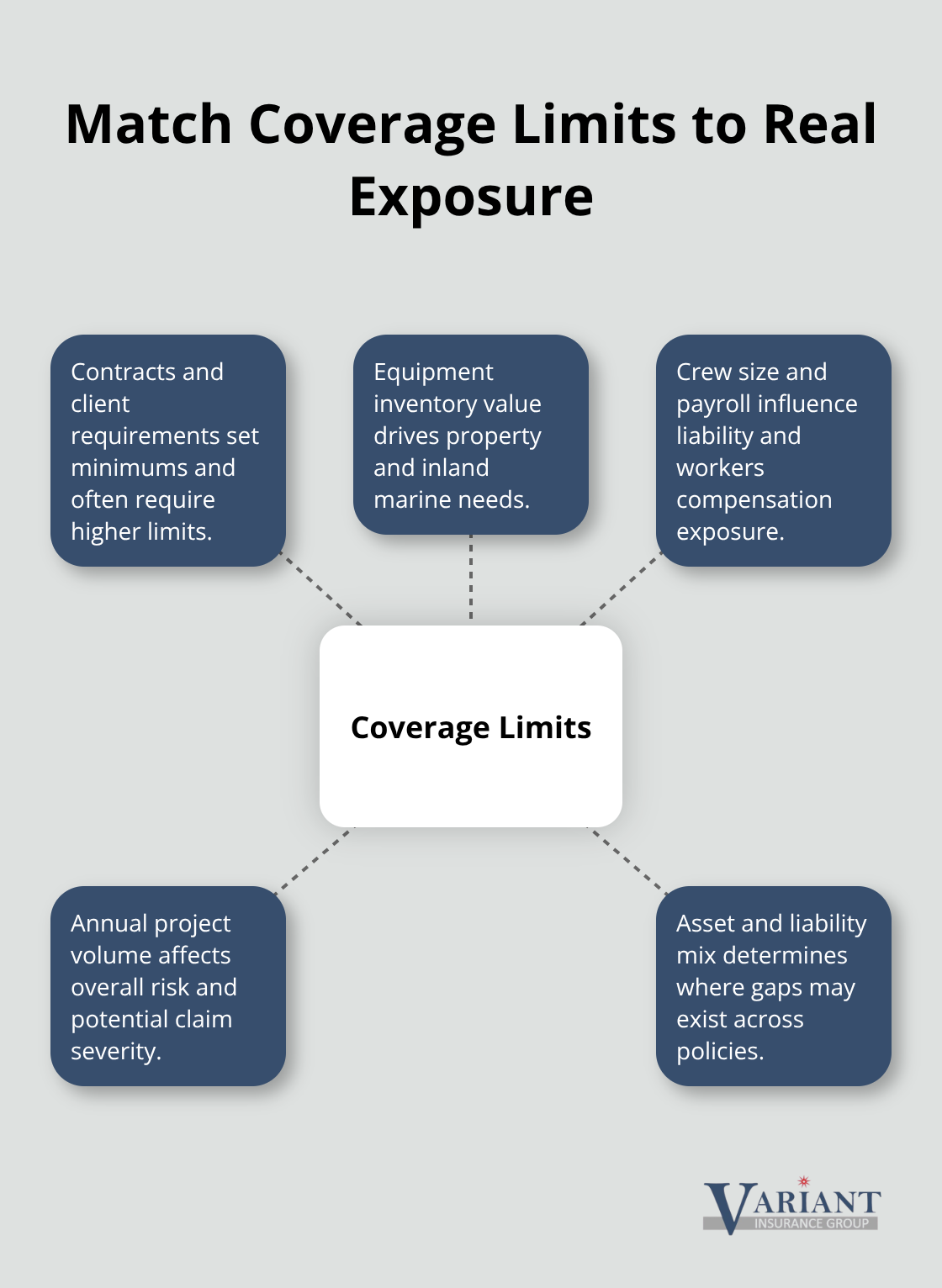

Matching Coverage Limits to Your Actual Exposure

Selecting the right coverage limits requires honest assessment of your project scope, contract obligations, and asset value rather than accepting default policy limits that competitors or brokers suggest. Your contracts with clients, your equipment inventory, and your typical crew size all shape what limits make sense for your operation. A contractor managing $5 million in annual projects needs different protection than one handling $500,000 in work.

The gap between underinsurance and appropriate coverage often appears only after a loss occurs-and by then, the financial damage is done. Understanding what each policy covers and where gaps exist positions you to make informed decisions about your protection strategy.

How to Build Safety Into Daily Operations

Identify Hazards Before Work Starts

Safety protocols only work when contractors embed them into daily operations rather than treating them as compliance checkboxes. Minnesota contractors who’ve reduced injury rates focus on three concrete practices: hazard identification before work starts, documented safety training that goes beyond annual refreshers, and accountability systems that tie safety performance to crew advancement and compensation.

MNOSHA’s Job Hazard Analysis requirement isn’t just paperwork-it’s a structured method to identify specific risks on each job, document controls, and communicate them to crews before equipment arrives. Contractors using JHA on every project phase report 30 to 40 percent fewer incident-related work stoppages compared to those using generic safety plans.

The difference lies in specificity: a site-specific safety manual that addresses carbon monoxide monitoring in enclosed spaces, walking surface hazards unique to your foundation work, and crane operations in Minnesota’s wind patterns protects crews far better than a template copied from five projects ago. Contractors who develop these manuals for each project phase catch risks that generic approaches miss.

Train Crews on Tasks, Not Just Compliance

Training should happen before work begins-not during a 15-minute orientation that workers forget by lunch. Effective contractors conduct toolbox talks tied directly to that day’s tasks: if crews work at height, the talk covers fall protection; if they operate equipment near utilities, it covers locating buried lines. MNOSHA data shows construction sites with documented daily pre-task planning and hazard awareness reduce recordable injuries by up to 50 percent.

Accountability matters equally-crews need to understand that safety violations carry consequences and that strong safety performance earns recognition or bonuses. Some Minnesota contractors tie crew leads’ advancement to safety metrics, ensuring leadership prioritizes prevention over schedule pressure.

Maintain Equipment on a Documented Schedule

Equipment maintenance and inspections prevent failures that injure workers and halt projects. A preventive maintenance schedule should cover cranes, hoists, derricks, and portable equipment on a documented timeline rather than waiting for breakdowns. MNOSHA requires warning signs at construction sites and specific equipment inspections; contractors who maintain records of completed inspections avoid citations and equipment-related injuries.

Regular inspections catch deterioration before it causes accidents. Contractors who document these inspections create a paper trail that protects their business legally and demonstrates due diligence to insurance carriers and clients.

Document Everything to Drive Continuous Improvement

Documentation transforms intentions into accountability. Project records should include safety committee meeting minutes, incident reports, training attendance logs, and equipment inspection dates. These documents protect your business legally if claims arise and provide data showing whether your safety investments are reducing injuries.

Contractors who review this documentation monthly can identify patterns-whether certain crews, equipment types, or project phases generate repeated incidents-and adjust controls accordingly. This approach turns safety from a cost center into a competitive advantage: lower injury rates mean lower workers compensation premiums, fewer project delays, and stronger client relationships.

Conclusion

Construction contractor risk management in Minnesota requires three interconnected elements: understanding your actual exposure, carrying appropriate insurance coverage, and embedding safety into how your crews work every day. The weather patterns, injury risks, and equipment losses outlined in this guide aren’t theoretical concerns-they’re predictable costs that contractors either manage proactively or absorb reactively through higher premiums, project delays, and lost profitability. Your general liability, workers compensation, and equipment coverage form the financial foundation that protects your business when incidents occur, while the safety protocols, hazard identification, and documented maintenance practices reduce the frequency and severity of losses that directly lower your insurance costs over time.

Contractors with strong safety records and minimal claims history pay substantially less for coverage than those treating risk management as optional. Start with an honest assessment of your current protection by reviewing your existing policies to identify gaps between what you think you’re covered for and what your policies actually protect. Evaluate your project contracts to confirm your coverage limits align with client requirements and your actual project values, then assess your safety practices to determine whether they’re genuinely preventing incidents or simply creating paperwork.

We at Variant Insurance Group work with Minnesota contractors to review these gaps and connect you with coverage that matches your specific operation. Contact Variant Insurance Group to discuss your contractor insurance strategy and ensure your protection keeps pace with your operation’s growth and changing project demands.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation