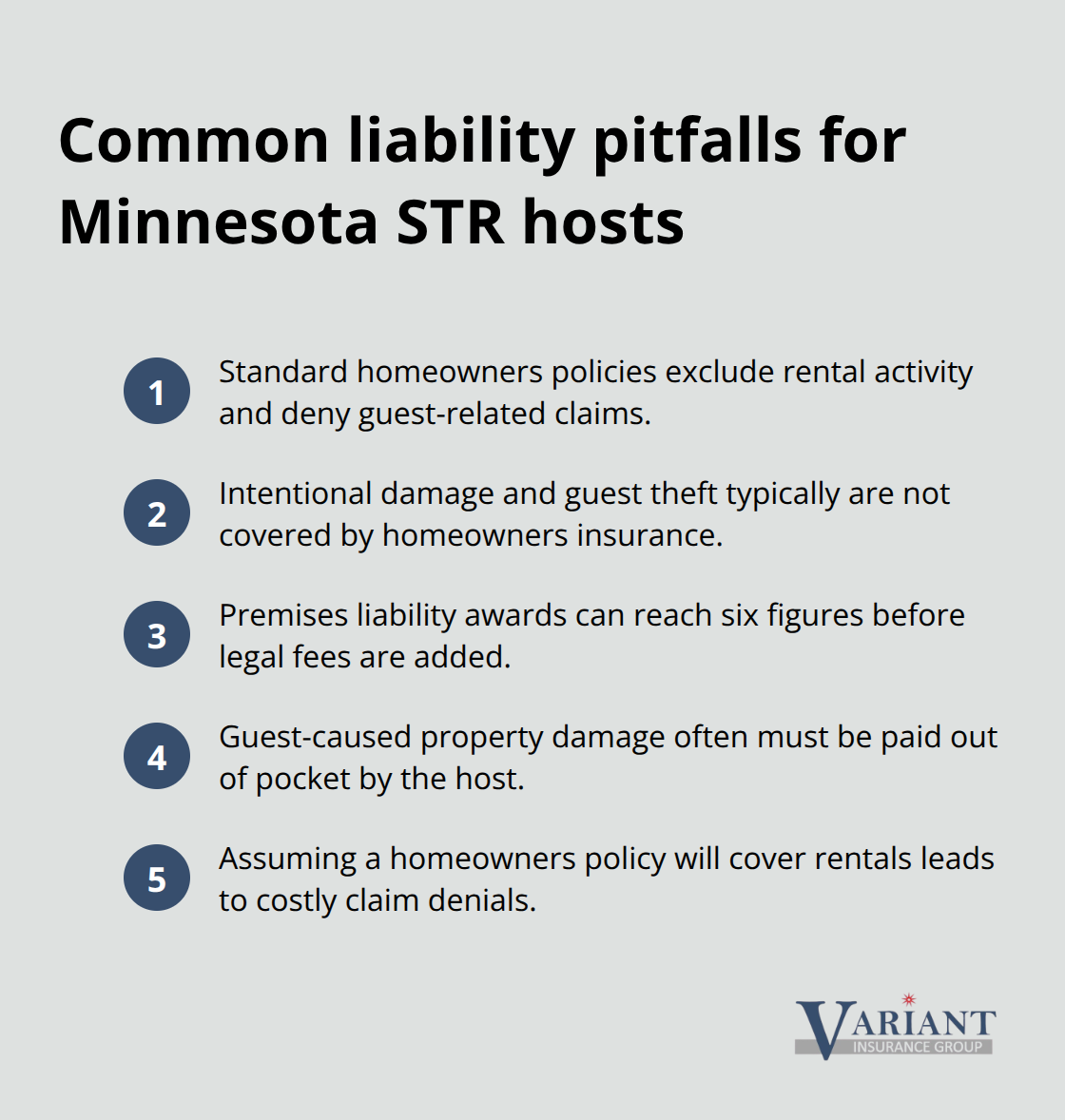

Short-term rental liability is one of the biggest blind spots for Minnesota hosts. Most people assume their homeowners insurance covers guest injuries or property damage, but standard policies explicitly exclude rental activity.

At Variant Insurance Group, we’ve seen hosts face six-figure lawsuits because they lacked proper coverage. The good news is that specialized short-term rental insurance exists to fill these gaps and protect both you and your guests.

What Liability Risks Do Short-Term Rental Hosts Actually Face

Guest Property Damage and Theft

Guest property damage claims hit Minnesota hosts harder than most realize. A broken hot tub, damaged furniture, or stained flooring costs $2,000 to $8,000 in repairs, but the real exposure comes from intentional damage or theft. Minnesota courts have awarded six-figure damages in premises liability cases tied to short-term rentals, and that’s before legal fees accumulate. Standard homeowners policies won’t cover any of this because they exclude rental activity entirely. If a guest steals your electronics, damages your kitchen, or vandalizes the property, you pay for every dollar out of pocket.

Most hosts get blindsided here-they assume their homeowners policy protects them until a claim gets denied.

Guest Injuries and Premises Liability

Guest injuries create even larger financial exposure. A visitor slips on your deck, falls down stairs, or gets injured by a faulty hot tub, and suddenly you face a lawsuit for medical bills, lost wages, and pain-and-suffering damages. Minnesota courts take premises liability seriously, which means injury claims can easily reach five or six figures. Your homeowners policy won’t cover this either because the injury occurred during a rental stay. The financial impact extends beyond the initial settlement-legal defense costs, court fees, and potential appeals drain resources quickly.

Local Regulations and Compliance Gaps

Local zoning and licensing requirements add another layer of responsibility. Operating without proper licensing or violating local short-term rental regulations eliminates liability protection entirely and exposes you to personal liability. The Minnesota Department of Commerce warns that relying on platform protection like Airbnb’s AirCover is dangerous-it functions as a reimbursement program with a 14-day claim deadline, not real insurance. You pay for repairs upfront and hope Airbnb approves your claim later. AirCover also excludes theft without forced entry, normal wear and tear, and intentional damage, leaving massive gaps in your protection.

Why Specialized Coverage Matters

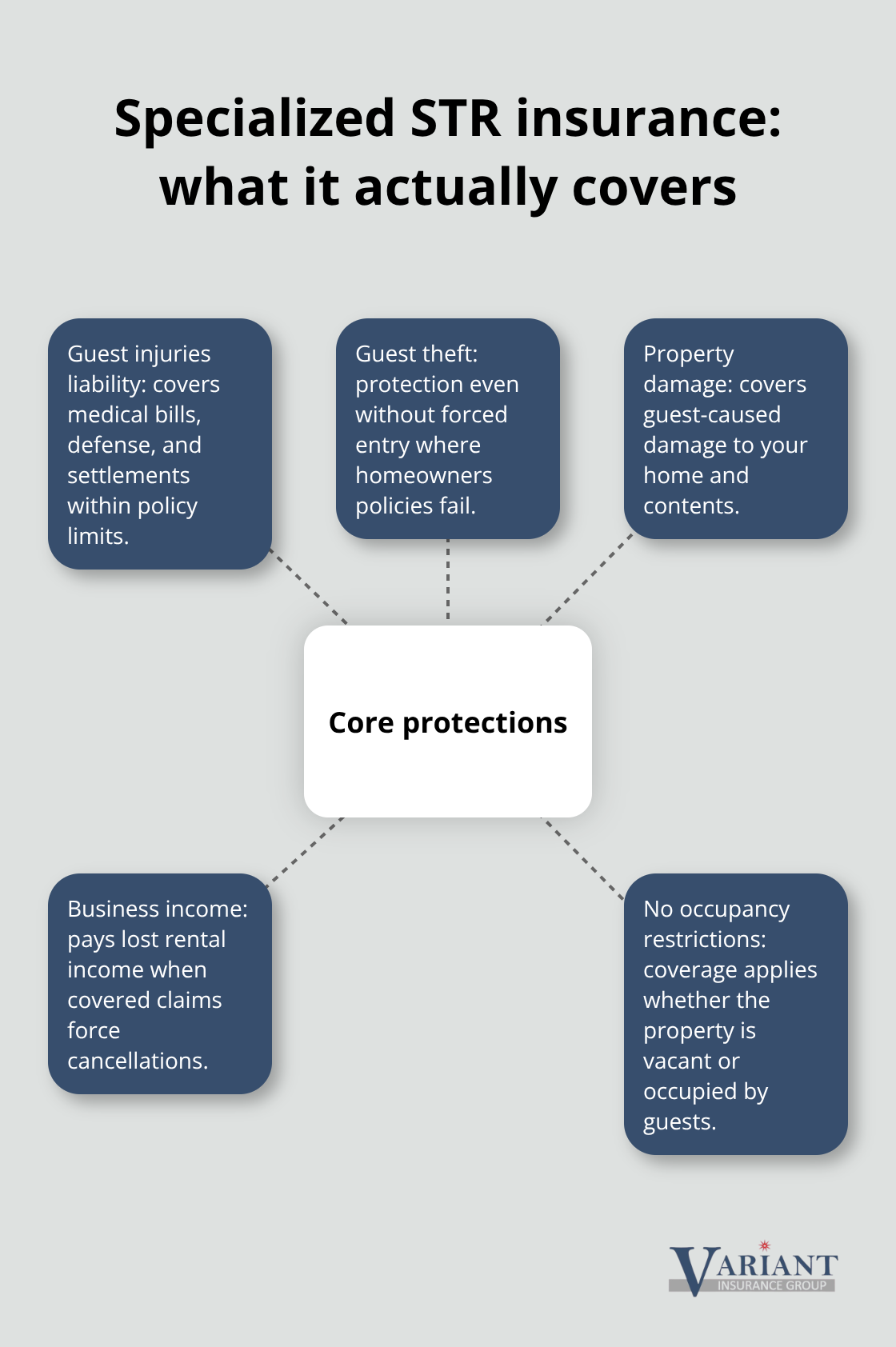

Specialized short-term rental insurance fills these holes by covering guest theft, property damage, guest injuries, and lost rental income with no occupancy restrictions. The cost typically ranges from $800 to $2,400 annually for Minnesota properties valued between $200,000 and $500,000, depending on location and amenities. Lake-area properties run 40 to 60 percent higher, while downtown Minneapolis properties are 25 to 35 percent higher. That premium costs far less than a single liability lawsuit.

Understanding which coverage options actually protect your property and income requires comparing what standard policies exclude against what specialized policies include.

What Coverage Actually Works for Minnesota Hosts

Why Standard Homeowners Insurance Fails

Standard homeowners insurance won’t protect your rental income or cover guest-related claims, which forces Minnesota hosts to choose between two paths: accept the risk and operate uninsured, or invest in specialized coverage designed for short-term rentals. Your homeowners policy explicitly excludes rental activity, meaning a guest injury, theft, or property damage claim gets denied immediately. Airbnb’s AirCover provides some baseline protection, but it operates as a reimbursement program with strict limitations. You must file claims within 14 days of checkout with photos and repair estimates, and the program excludes theft without forced entry, mold, intentional damage, and normal wear and tear. For Minnesota hosts, this creates a dangerous gap. A guest steals your laptop, damages your kitchen cabinets, or injures themselves on your deck, and AirCover denies the claim because it falls outside their narrow coverage. You pay thousands out of pocket.

Specialized Short-Term Rental Insurance Closes the Gaps

Specialized short-term rental insurance closes these gaps entirely. Policies from carriers like Proper Insurance cover guest theft without forced entry, property damage from guests, guest injuries on your property, and lost rental income if a covered claim forces you to cancel bookings. The cost ranges from $800 to $2,400 annually for Minnesota properties valued between $200,000 and $500,000, depending on location and guest turnover. Downtown Minneapolis properties typically cost 25 to 35 percent more than suburban properties, while lake-area rentals run 40 to 60 percent higher due to increased liability exposure from water amenities and higher property values.

Essential Add-On Coverages That Matter

Additional liability protection strengthens your position further. Amenity liability coverage explicitly includes hot tubs, pools, kayaks, and other on-site or off-site equipment that standard homeowners policies ignore. If a guest injures themselves using your hot tub or damages your kayak, specialized coverage protects you while standard policies leave you exposed. Business revenue protection pays actual lost income if a covered claim prevents you from renting, with no time limit on recovery. A kitchen fire, burst pipe, or serious guest injury can force you to cancel bookings for weeks. AirCover won’t cover this lost income, but specialized policies do. Property entrustment coverage protects against guest theft and vandalism, addressing the exact scenarios where homeowners policies fail. Liquor liability coverage is also essential for Minnesota hosts who allow guests to bring alcohol or provide it as an amenity. Guest injuries involving alcohol create substantial liability exposure, and standard policies exclude this risk entirely.

Deductibles and Premium Decisions

When comparing policies, focus on deductibles carefully. A $500 deductible costs more annually than a $1,000 deductible, but you pay less per claim. For properties over $300,000, very high deductibles should be avoided because guest damage claims happen frequently and quickly deplete your savings. Work with an independent insurance agent to compare quotes from multiple carriers and identify which coverage gaps matter most for your specific property and guest patterns. The right policy aligns your protection with your actual exposure, not just the lowest premium.

How Liability Coverage Protects Hosts and Guests

Specialized short-term rental insurance transforms your financial exposure from unlimited to manageable. When a guest injures themselves on your property or causes serious damage, the right policy covers your legal defense, settlement costs, and any judgments against you up to your policy limits. Minnesota courts have awarded six-figure damages in premises liability cases, which means a single incident can bankrupt an uninsured host. With coverage in place, your insurer handles the claim investigation, negotiates with the injured party, and covers legal fees regardless of the outcome. This protection extends to your rental income as well. If a covered claim forces you to cancel bookings while repairs happen, business revenue protection pays your actual lost income with no time limit. A water pipe burst in January could cancel reservations for two weeks or more, costing you $3,000 to $6,000 in lost bookings depending on your nightly rate. Without this coverage, that income vanishes entirely. Platform protection like Airbnb’s AirCover functions as a reimbursement program only, meaning you front the money and wait for approval. Specialized policies work differently by covering costs directly through your insurer’s claims team.

Guest Injuries Create Immediate Financial Liability

Guest injuries on your property trigger immediate financial liability. A visitor slips on wet deck boards, falls down stairs, or gets injured by a faulty hot tub and suddenly faces medical bills, lost wages, and pain-and-suffering claims. Your specialized policy covers medical expenses for guest injuries up to your selected limits, typically starting at one million dollars in liability protection. More importantly, your insurer’s legal team handles the entire claim rather than forcing you to navigate the process alone. They coordinate with the injured party’s attorney, negotiate settlements, and defend you in court if necessary. This professional handling speeds resolution and prevents emotional or financial mistakes during negotiations. Policies from carriers like Proper Insurance include dedicated claims support with in-house expertise for short-term rental scenarios, which matters because your claims adjuster understands vacation rental liability rather than treating it like a standard homeowners claim.

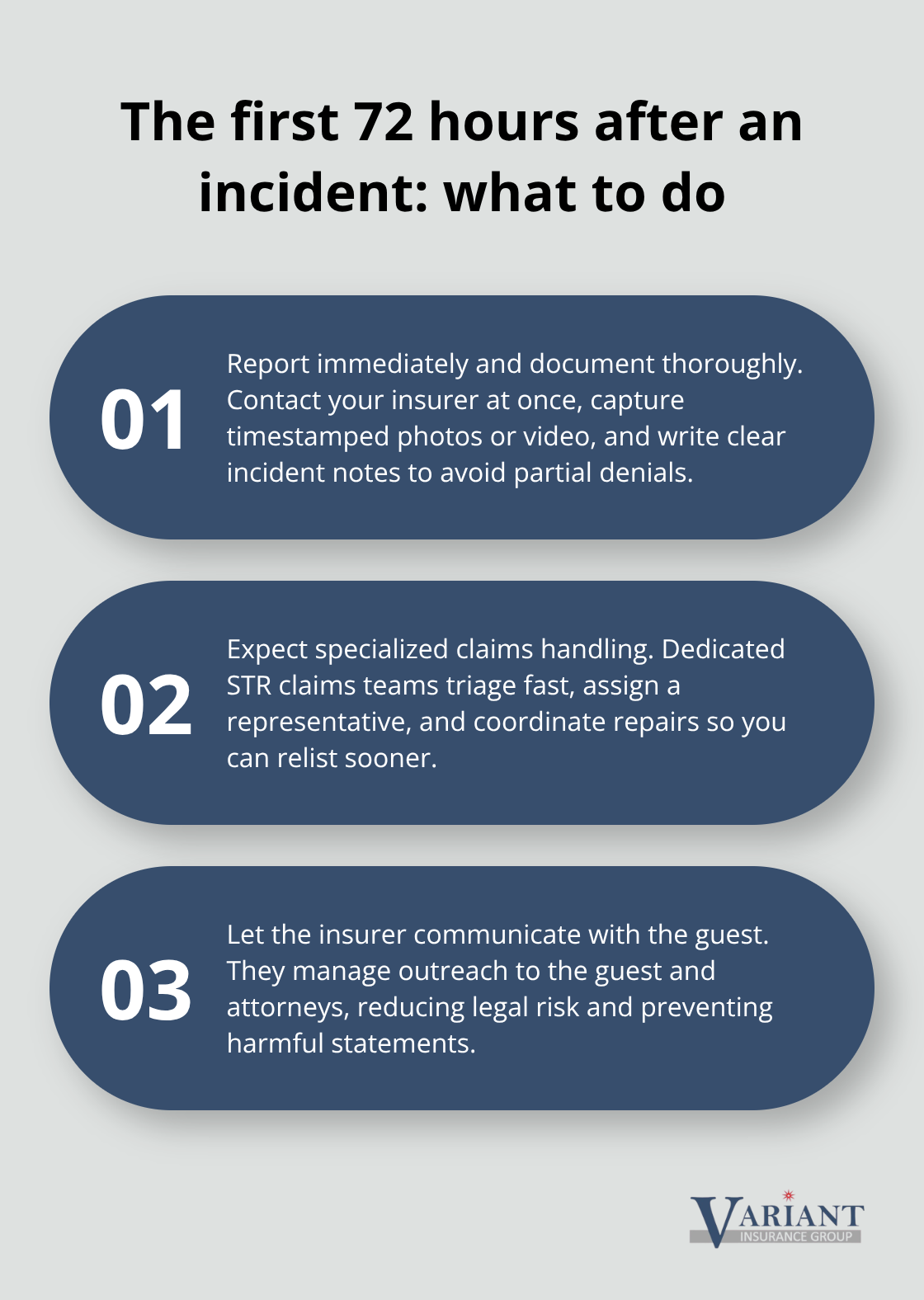

The First 72 Hours Determine Claim Approval

The first 72 hours after an incident determine whether your claim gets approved or denied. Prompt notification to your insurer, documented photos of damage or injuries, and accurate incident details make the difference between full coverage and a partial denial. Specialized short-term rental insurers understand this timeline and staff their claims departments accordingly.

When you contact your carrier with a guest injury or property damage claim, a dedicated claims representative begins investigating immediately rather than routing your claim through a general homeowners queue. This responsiveness matters because your rental property generates daily income and every day offline costs money. A fast claims process gets your property repaired, relisted, and generating revenue again within days rather than weeks. Your insurer also handles communication with the guest and their legal representatives, protecting you from saying something that damages your position. Standard homeowners insurance companies rarely have claims staff trained in short-term rental liability, which means your claim gets processed slowly or incorrectly. Specialized carriers have processed hundreds of short-term rental claims and know exactly which documentation matters, which coverage applies, and how quickly to move toward resolution.

Final Thoughts

Short-term rental liability protection separates sustainable Minnesota hosts from those operating on borrowed time. Standard homeowners insurance explicitly excludes rental activity, and Airbnb’s AirCover functions as a reimbursement program with strict deadlines and significant gaps, leaving you personally liable for claims that reach six figures. Specialized coverage designed for short-term rentals closes these gaps by protecting guest injuries, property damage, theft without forced entry, lost income, and amenities that standard policies ignore entirely.

For Minnesota properties valued between $200,000 and $500,000, premiums typically range from $800 to $2,400 annually-a modest investment compared to a single lawsuit. Lake-area and downtown Minneapolis properties cost more due to higher liability exposure, but the protection remains essential regardless of location. Your claims experience matters equally; specialized carriers staff their departments with short-term rental expertise, meaning professionals who understand vacation rental liability handle your incident rather than treating it like a standard homeowners claim.

We at Variant Insurance Group shop Minnesota’s top-rated insurance companies to find the perfect short-term rental insurance policy for your specific property and guest patterns. Our team compares coverage options, deductibles, and premiums across multiple carriers so you get the protection you need at the right price. Contact us today to evaluate your rental property insurance and close the gaps that leave you exposed.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation