Running a small business in Minnesota means managing countless moving parts. Your vehicles are essential to operations, but personal auto insurance won’t protect your business when they’re used commercially.

At Variant Insurance Group, we help Minnesota small business owners find coverage that actually fits their needs. The right commercial auto policy shields you from liability, covers vehicle damage, and keeps your operation compliant with state law.

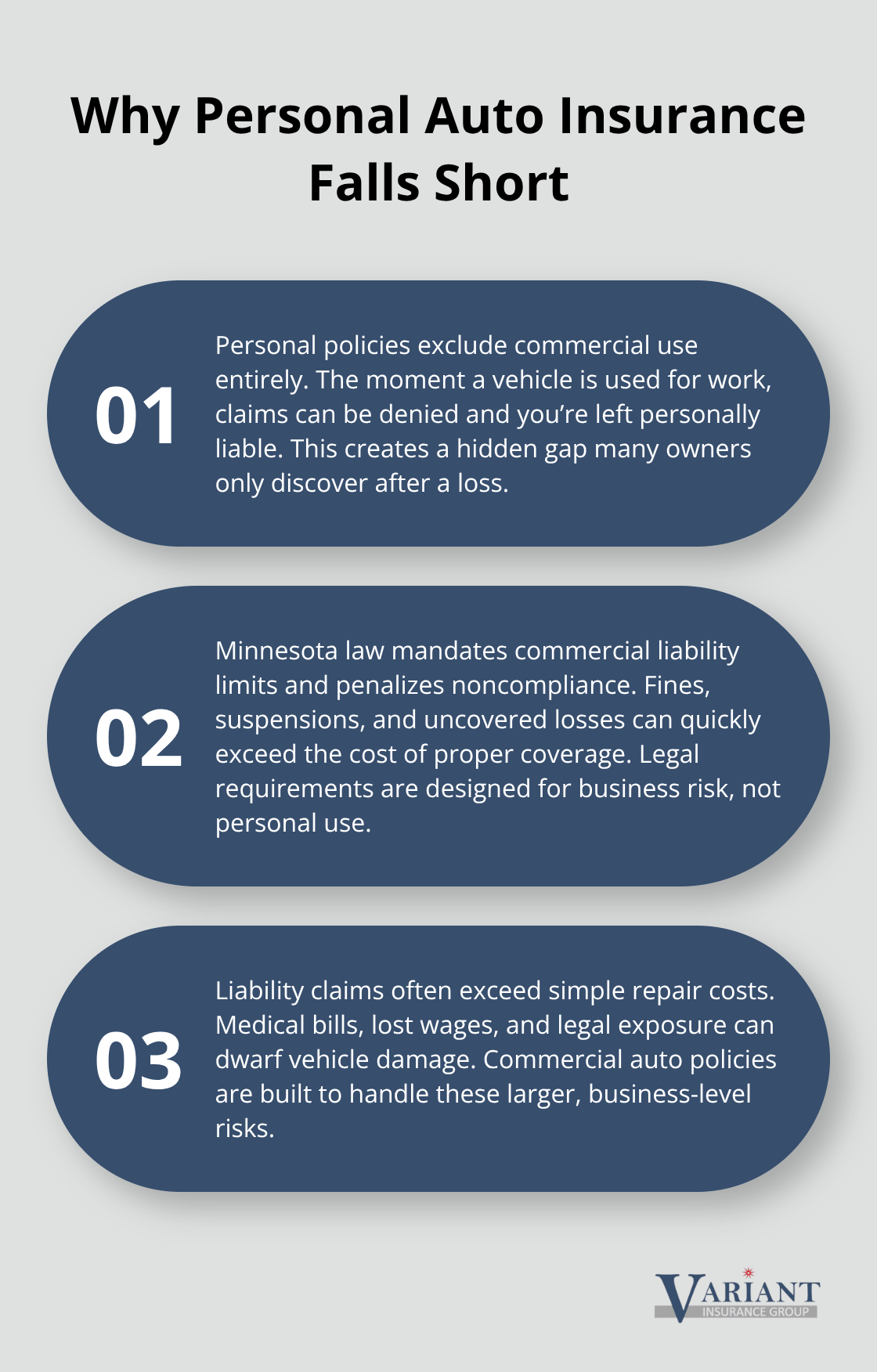

Why Personal Auto Insurance Falls Short for Business

Personal Policies Exclude Commercial Use Entirely

Personal auto policies explicitly exclude commercial use, leaving you with zero coverage the moment your vehicle operates for work purposes. If an accident occurs during a business trip, your insurer can deny the claim entirely and leave you personally liable for damages, medical bills, and legal costs. This gap exposes your business to catastrophic financial risk that most small business owners don’t anticipate until it’s too late.

Minnesota’s Legal Requirements Demand Commercial Coverage

Minnesota law requires all business vehicles to carry commercial auto insurance with minimum liability limits of 30/60/10 ($30,000 per person and $60,000 per accident in bodily injury coverage, plus $10,000 in property damage). Operating without it carries a $200 fine minimum, plus license and vehicle registration suspension for up to 30 days. Beyond legal compliance, the financial exposure is staggering-a single accident with injuries can easily exceed $100,000 in medical costs and property damage.

If you’re personally liable because your insurance won’t cover it, creditors can pursue your business assets and personal savings. Minnesota’s no-fault system requires you to exhaust your Personal Injury Protection (PIP) benefits first, but only commercial policies include the required coverage that protects both you and your employees regardless of fault.

Liability Claims Threaten More Than Vehicle Damage

A liability claim isn’t just about vehicle repairs. If someone is injured in an accident you cause, their medical bills, lost wages, and pain-and-suffering damages can dwarf the cost of repairs. Commercial auto liability covers these costs up to your policy limits, but most Minnesota small businesses operate with only the legal minimum, which is inadequate.

Many contracts and certificates of insurance now require $1,000,000 in combined single limit (CSL) coverage, far exceeding the state minimum. Without this coverage, you lose business opportunities and remain exposed to claims that exceed your limits. Uninsured and underinsured motorist protection closes another critical gap by covering your own medical expenses and vehicle damage when the other driver is at fault but lacks sufficient insurance-especially important in Minnesota, where many drivers carry only minimum limits.

Physical Damage Coverage Protects Your Assets

Physical damage coverage (collision and comprehensive) protects your vehicles from accidents, theft, weather, and vandalism. This matters significantly if your vehicles are financed or leased, as most lenders require this coverage as a condition of the loan. Without it, you absorb the full cost of repairs or replacement, which can cripple cash flow for small operations.

The right commercial auto policy addresses all these gaps at once. Understanding what types of coverage actually exist-and which ones fit your specific fleet-is the next step toward protecting your Minnesota business.

Types of Commercial Auto Coverage for Minnesota Businesses

Commercial Auto Liability Insurance Protects Against At-Fault Claims

Commercial auto liability insurance covers medical expenses and property damage when you cause an accident, and Minnesota law mandates it for all business vehicles. The state minimum stands at 30/60/10 ($30,000 per person, $60,000 per accident in bodily injury, plus $10,000 property damage), but that limit proves dangerously low for most operations. A single injury claim easily exceeds $100,000, and commercial auto insurance policies have higher liability limits, for example $1 million. Construction contractors average around $264 per month for commercial auto, partly because their liability risk substantially outpaces office-based operations. Contractors frequently cause property damage during job-site access or while loading materials, and those claims accumulate quickly. Real estate agents and delivery services face similar pressures. The practical approach involves exceeding the minimum by at least $500,000-many Minnesota small businesses find that $1,000,000 CSL costs only 15–25% more than minimum limits but eliminates the stress of underinsurance.

Collision and Comprehensive Coverage Protect Your Vehicle Assets

Physical damage coverage splits into collision and comprehensive, and this distinction shapes your protection significantly. Collision covers accidents and crashes; comprehensive covers theft, vandalism, weather, and fire. If your vehicles are financed or leased, your lender mandates both. If you own them outright, many owners skip comprehensive to save money-a mistake when Minnesota experiences regular hail storms and vehicle theft remains common in urban areas. The real cost driver isn’t the basic liability-it’s how you layer physical damage and motorist protections on top of your foundation coverage.

Uninsured and Underinsured Motorist Protection Closes a Critical Gap

Uninsured and underinsured motorist protection is the coverage type most Minnesota small business owners overlook entirely, yet it proves essential. Minnesota operates as a no-fault state, meaning your Personal Injury Protection covers your medical costs first, but if the other driver is at fault and lacks sufficient insurance, uninsured motorist coverage protects you and your employees from that gap. This protection activates when the at-fault driver carries inadequate limits or no insurance at all-a common scenario in Minnesota, where many drivers carry only minimum coverage.

Real-World Premium Costs for Minnesota Small Businesses

Data from Insureon shows that among Minnesota small-business customers, roughly 40% pay less than $200 monthly for commercial auto, indicating that affordable coverage exists if you structure it correctly. A solo contractor with one vehicle typically pays $1,500–$4,000 annually for solid coverage including $1,000,000 liability, collision, comprehensive, and uninsured motorist protection.

A three-vehicle local-service operation runs $5,000–$15,000 yearly depending on driver history and mileage. The key involves matching coverage to actual risk, not defaulting to minimum limits or skipping physical damage to save a few dollars monthly.

Once you understand what coverage types exist and how they fit your fleet, the next step is selecting the right policy structure and deductible levels that balance affordability with genuine protection.

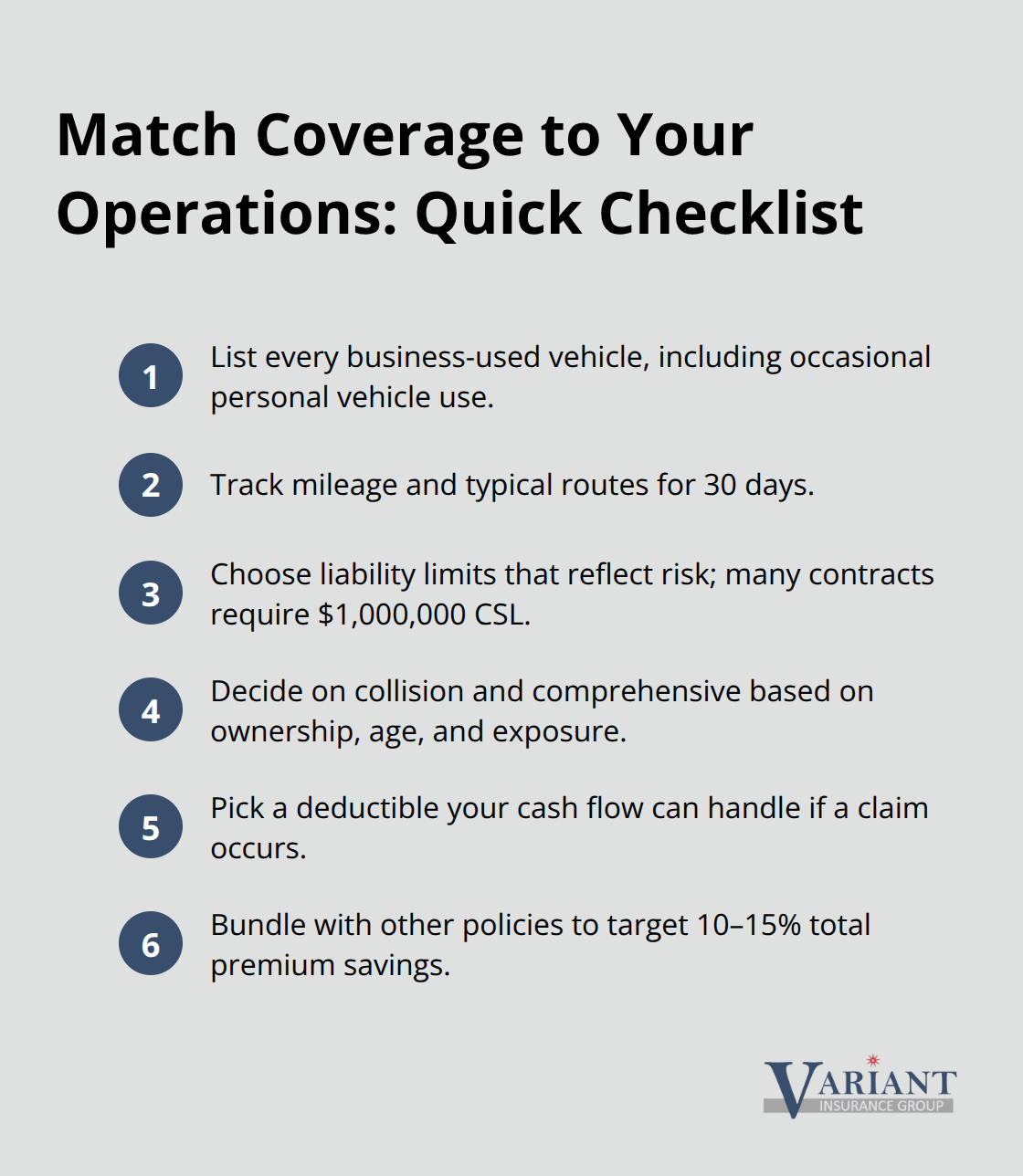

How to Match Coverage to Your Business Operations

List Every Vehicle and Document Actual Usage

The mistake most Minnesota small business owners make is treating commercial auto insurance like a checkbox task instead of a strategic decision tied directly to how their vehicles operate. Start by listing every vehicle used for business, including part-time use of personal vehicles by employees. A plumber with one van faces completely different risk than a delivery service with five box trucks, and a real estate agent using a personal sedan occasionally differs from both.

Next, calculate your annual mileage and typical routes. A contractor who operates within a 15-mile radius of the office has lower risk than one traveling three states for jobs, and that difference directly affects your premium and required coverage limits. Many Minnesota small businesses discover during this exercise that they’ve been insuring vehicles for work that no longer serve business purposes, or conversely, they’re using uninsured personal vehicles for occasional work trips. The practical approach involves documenting actual usage patterns for 30 days, then matching that reality to your policy structure.

Select Physical Damage Coverage Based on Vehicle Ownership

Coverage selection depends entirely on what you’re protecting. If your vehicles are financed or leased, collision and comprehensive coverage is mandatory, not optional, so your monthly cost includes these from the start. If you own vehicles outright, most Minnesota business owners should still carry comprehensive coverage given the frequency of hail storms and vehicle theft in urban areas, though collision becomes a choice based on vehicle age and value.

Choose Liability Limits That Match Your Risk Exposure

The real decision point involves your liability limits and motorist protection. Among Insureon customers in Minnesota, most small businesses find that jumping from the legal minimum of 30/60/10 to $1,000,000 combined single limit costs only 15–25% more monthly but eliminates catastrophic underinsurance risk. For construction contractors averaging $264 monthly for commercial auto, that increase amounts to roughly $40–$66 per month for substantially better protection. Many contracts and certificates of insurance now require $1,000,000 in combined single limit coverage, far exceeding the state minimum.

Balance Your Deductible Against Cash Flow Capacity

Your deductible choice shapes affordability directly: a $1,000 deductible costs roughly 15–20% less than a $500 deductible, but you must be certain your business can absorb that out-of-pocket cost if a claim occurs. Many Minnesota small business owners choose $750 as a middle ground, balancing monthly savings against realistic cash flow capacity. This decision requires honest assessment of your business’s financial reserves rather than simply selecting the lowest premium option.

Leverage Bundling and Discounts to Lower Total Cost

Compare what discounts actually apply to your situation. Bundling commercial auto with general liability or property coverage typically saves 10–15% on your total premium, which often matters more than individual policy discounts. Fleet size, safety equipment, and clean driving records can also reduce costs. At Variant Insurance Group, we shop Minnesota’s top-rated carriers to find the combination of coverage, deductible, and bundling that fits your actual operations and budget.

Final Thoughts

Commercial auto liability, physical damage coverage, and uninsured motorist protection form the foundation of any Minnesota small business auto policy that actually works. Most Minnesota small business owners discover that jumping from legal minimums to $1,000,000 in combined single limit coverage costs only 15–25% more monthly while eliminating the stress of underinsurance. That modest increase in premium translates directly into genuine peace of mind and protection for your operation.

The next step involves gathering details about your vehicles, drivers, and routes, then obtaining quotes from multiple carriers to compare actual costs. Many Minnesota small businesses find that bundling commercial auto with general liability or property coverage saves 10–15% on total premiums. Once you’ve selected coverage that fits your operations, activation happens within 24 hours, and a certificate of insurance arrives immediately as proof of coverage.

At Variant Insurance Group, we shop Minnesota’s top-rated carriers to find the combination of coverage, deductible, and bundling that fits your actual operations and budget. Contact us today to discuss your Minnesota small business auto insurance needs and find the affordable, reliable coverage your operation deserves.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation