Your homeowners and auto insurance policies have limits. When a lawsuit or major accident exceeds those limits, your personal assets are at risk.

At Variant Insurance Group, we help Minnesota residents understand how personal umbrella insurance quotes reveal the extra protection layer you need. This guide walks you through comparing quotes, spotting real savings, and securing coverage that actually fits your situation.

What Umbrella Insurance Actually Protects

How Umbrella Coverage Fills the Gap

Personal umbrella insurance sits on top of your homeowners and auto policies, activating when damages exceed what those underlying policies cover. If you face a $1.5 million lawsuit but your homeowners policy caps liability at $300,000 and your auto policy at $250,000, you’re $950,000 short-money that comes directly from your savings, investments, and other assets. Umbrella coverage pays the difference up to your policy limit, typically starting at $1 million. This protection layer exists because standard policies alone leave dangerous gaps. Homeowners insurance typically maxes out liability at $300,000, and auto policies at $250,000 or $500,000. One multi-vehicle accident or serious injury on your property can exceed those limits instantly.

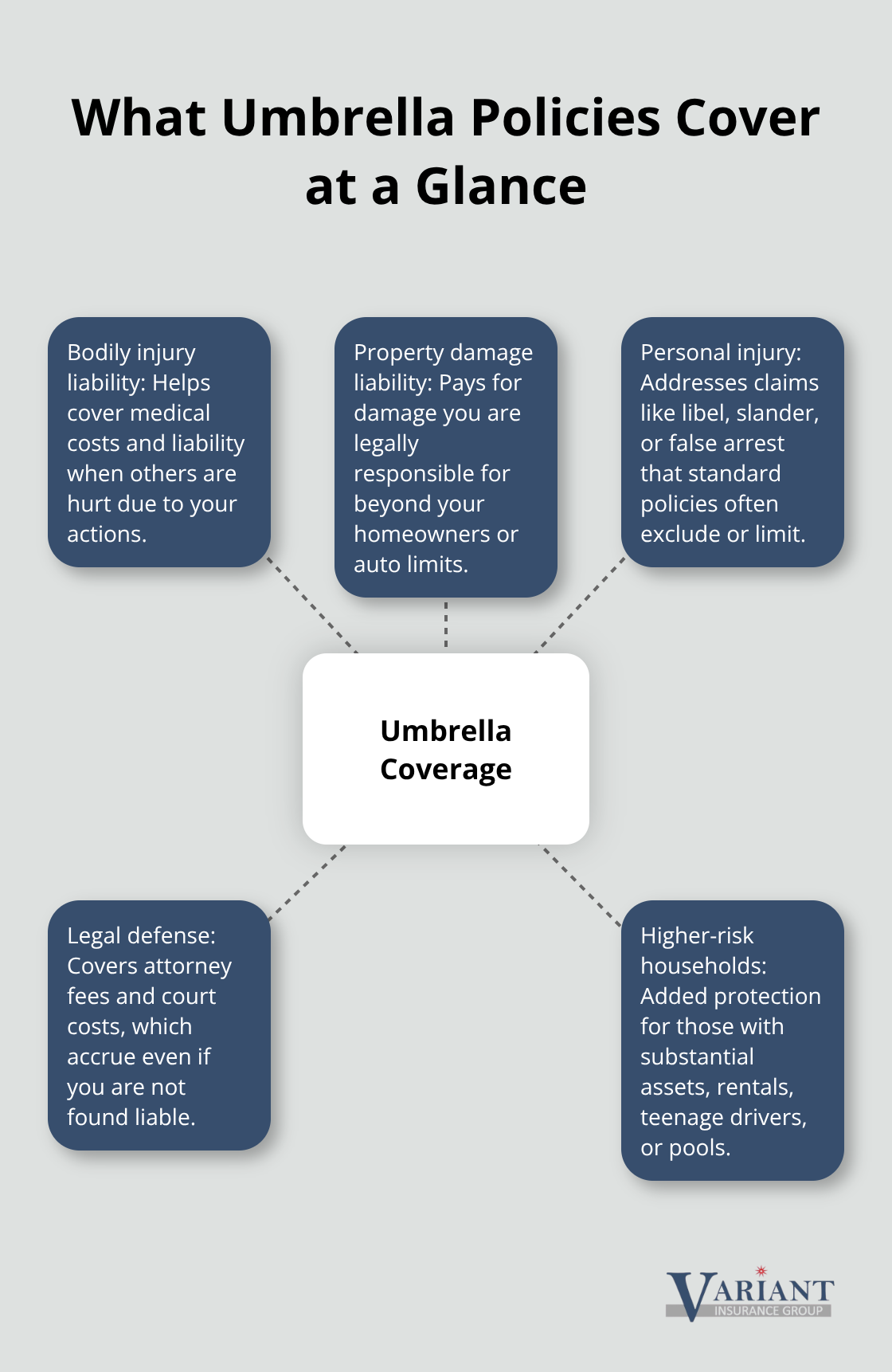

What Claims Umbrella Policies Actually Cover

The protection extends well beyond simple accidents. Umbrella policies cover bodily injury claims, property damage liability, and personal injury lawsuits involving libel, slander, or false arrest-claims that standard homeowners and auto policies often exclude or limit significantly. They also pay legal defense costs and court fees, expenses that accumulate even when you’re not found liable. These attorney bills and court costs protect your liquid assets from draining away during litigation. Minnesota residents with substantial assets, rental properties, teenage drivers, or pools face real exposure that umbrella insurance addresses directly.

The Real Cost of Protection

The price point surprises most people. A $1 million umbrella policy runs roughly $200–$400 annually, while $2 million coverage averages $600–$1,000 per year. That’s a small premium relative to the protection you gain. Higher limits exist too; some carriers offer $5 million or more coverage. The key is matching your umbrella limit to your actual assets. Add up your home equity, savings, investments, and retirement accounts to determine how much exposure you have, then select a limit that covers that amount plus potential future earnings.

Understanding what umbrella insurance covers helps you recognize whether your current protection is adequate. The next step involves comparing actual quotes from multiple insurers to see how coverage options and pricing vary based on your specific situation.

Comparing Quotes from Multiple Insurers

Why Shopping Multiple Carriers Matters

You need quotes from at least three different insurers if you want to find real savings on umbrella coverage. The pricing differences are substantial. A $1 million policy might cost $250 annually from one carrier and $400 from another, even when the underlying coverage is identical. Minnesota residents often assume their current homeowners or auto insurer will offer the best umbrella rates, but that assumption frequently fails. Clients regularly save money by shopping beyond their existing carrier. Start by requesting quotes from your current insurer, then contact two or three additional providers to establish a true comparison.

Gathering the Information Insurers Need

When you request quotes, you’ll provide your ZIP code, existing auto and homeowners policy limits, and information about drivers in your household. Most insurers now offer online quote tools that take 5-10 minutes to complete, though calling an agent yields more detailed conversations about your specific situation. The quote process reveals something critical: many insurers require minimum underlying coverage limits before they’ll sell you umbrella protection. Common minimums are $250,000 bodily injury per person and $500,000 per accident on auto, plus $300,000 liability on homeowners. If your current policies fall below these thresholds, you’ll need to increase those limits first, which affects your total cost calculation.

How Deductibles and Bundling Affect Your Price

The deductible structure matters more than most people realize. Some umbrella policies have a zero deductible, meaning coverage activates immediately once your underlying policy limits are exhausted. Others impose a $5,000 or $10,000 retained limit, which you pay before umbrella coverage activates. A higher deductible typically lowers your premium by 10-15%, but that savings only makes sense if you can actually afford to pay that deductible during a claim. Bundling your umbrella with existing auto and homeowners policies at the same insurer typically delivers a 5-10% discount across your entire package. However, bundling locks you into one carrier for multiple policies, which reduces your flexibility if that insurer raises rates or service quality declines. Some carriers like RLI offer standalone umbrella policies, meaning you don’t need to move your home and auto insurance to get their umbrella coverage.

Claims History and Driver Profile Impact on Rates

Your claims history directly influences pricing. One prior liability claim can increase your umbrella premium by 25-40%, while clean records receive the best rates. The number of drivers covered also matters; households with teenage drivers pay substantially higher premiums because younger drivers represent elevated risk. Comparing quotes requires you to keep the coverage limit constant across all providers. Compare $1 million to $1 million, not $1 million from one insurer to $2 million from another. Look at the total annual cost, not just the umbrella premium in isolation. Your bundled discount with one carrier might make their higher base rate cheaper overall than a competitor’s standalone umbrella price.

Making Your Comparison Count

The real work begins once you have three or more quotes in hand. Line them up side by side with identical coverage limits and deductible amounts. Note which carriers require you to maintain minimum underlying limits and which ones offer flexibility. Pay attention to whether each quote includes bundling discounts and what those discounts actually cover. Some insurers discount only the umbrella premium, while others apply savings across your entire policy package. This comparison process exposes which carriers truly compete for your business and which ones price aggressively only for new customers. Once you understand how quotes differ and what drives those differences, you can evaluate which coverage options actually align with your assets and risk profile.

How to Actually Cut Your Umbrella Insurance Costs

Bundling Policies Without Overpaying

Bundling your umbrella policy with existing auto and homeowners coverage at the same insurer typically saves 5-10% across your entire package, but this discount only works if that carrier offers competitive rates on all three policies. Many Minnesota residents lock into bundling without checking whether their current insurer actually prices those underlying policies competitively. The math matters here: a $50 monthly discount on bundling means nothing if your auto insurance costs $40 more per month than a competitor charges. We recommend running quotes on your complete policy package, not just the umbrella premium. Some carriers like RLI deliberately offer standalone umbrella policies because they understand that bundling discounts can trap customers into overpaying on their base coverage.

Raising Underlying Limits to Lower Umbrella Premiums

Increasing your underlying homeowners and auto liability limits before purchasing umbrella coverage sounds counterintuitive for saving money, yet it frequently reduces your total umbrella cost. Insurers price umbrella policies partly based on the underlying limits you carry. Higher underlying limits mean fewer claims will exceed those thresholds and trigger umbrella coverage, so insurers charge lower premiums. Moving your homeowners liability from $300,000 to $500,000 and your auto liability from $250,000 to $500,000 per accident might cost an extra $30-$50 monthly across those policies, but it can lower your umbrella premium by $200-$300 annually. The net result is savings.

Protecting Your Claims History

Minnesota residents with clean claims histories receive the best umbrella rates. One previous claim can increase your premium by 25-40%, making claims prevention your most powerful cost lever. This means documenting safety measures on your property matters: fence maintenance records, pool inspection documentation, and dog behavior training receipts all support your case for lower rates. A household with one prior liability claim might qualify for a $1 million umbrella at $350 annually, while that same household with a clean record qualifies at $200 annually. The difference compounds over years. If you’re considering filing a claim for minor property damage, calculate whether the premium increase over the next 3-5 years exceeds what you’d recover from insurance. For small claims under $5,000, skipping the claim and paying out of pocket often costs less than the resulting rate increases.

Managing Household Driver Risk and Deductibles

The number of drivers in your household directly affects pricing, with teenage drivers triggering substantially higher premiums because they represent elevated accident risk. Minnesota insurance data shows that households with drivers under age 25 pay 30-50% more for umbrella coverage. If your household includes a teenage driver, shopping for umbrella quotes before that driver reaches age 21 versus after age 25 creates a measurable difference in available rates. The deductible structure on your umbrella policy also influences your annual cost. A zero deductible costs more than a $5,000 or $10,000 retained limit, typically reducing premiums by 10-15% when you accept that higher deductible. This choice depends on your liquid assets. If you have $50,000 in savings and face a $500,000 lawsuit, you can afford a $10,000 deductible. If you have $10,000 in savings, a zero deductible protects you from being unable to pay that retained amount when a claim occurs.

Finding Insurers Who Compete for Your Risk Profile

The comparison process exposes which carriers price aggressively for your specific risk profile. Some insurers compete hard for families with teenagers because they’ve found lower claims rates within that group. Others price them out of their market. Shopping multiple carriers reveals which insurer actually wants your business at a competitive rate, rather than assuming your current provider offers the best deal.

Final Thoughts

Comparing personal umbrella insurance quotes across multiple carriers reveals that protection gaps exist in nearly every Minnesota household, and the cost to fill those gaps runs far smaller than most people expect. A $1 million umbrella policy costs roughly $200–$400 annually, yet it shields everything you’ve built from a single lawsuit that exceeds your underlying policy limits. That’s not an expense; it’s a safeguard that protects your assets from catastrophic loss.

The process itself teaches you something valuable about your current coverage. When insurers require minimum underlying limits before selling umbrella protection, you discover whether your homeowners and auto policies are actually adequate. Many Minnesota residents find that raising those underlying limits to meet umbrella eligibility requirements costs less than they expected, and the resulting umbrella premium drops because higher underlying limits reduce insurer risk. Your claims history and household driver profile directly determine your available rates-a clean record qualifies you for substantially better pricing than one prior liability claim, making prevention your most powerful cost lever.

We at Variant Insurance Group work with Minnesota residents to compare personal umbrella insurance quotes across top-rated carriers and identify which coverage actually fits your situation. Contact us to review your quotes and confirm you’re getting the protection and pricing your assets deserve.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation